Looming Market Crashes

June 2, 2026

Our Financial Markets and Their Many Irrationalities

I launched my American Pravda series a decade ago next month. My conscious strategy was quite unusual, being almost exactly the opposite of that followed by nearly everyone else covering those same controversial topics.

As some of them explicitly told me, they had always deliberately avoided exploring too many different and unrelated historical controversies. Instead, they believed that they were on safer ground by confining their work to a relatively narrow slice of these.

So some of them spent years challenging the official narrative on World War II or the JFK Assassination or the 9/11 Attacks or took other positions denigrated as “conspiracy theories” by our political and media establishments. But they usually focused on just one or two of those major issues, and ignored the others.

#butGod: The Power of ...

Check Amazon for Pricing.

#butGod: The Power of ...

Check Amazon for Pricing.

I decided to take the opposite approach and cover as many of those as possible. After years of effort, my American Pravda series has now done this, constituting a broader collection of such material than anything else I’ve encountered on the Internet.

- The American Pravda Series

Ron Unz • The Unz Review • 146 Articles • 1,230,000 Words

In an October 2016 article, I’d sketched out the reasoning behind my contrary approach:

Individuals who challenge the prevailing media narrative with unorthodox ideas are often reluctant to raise too many such controversial claims simultaneously lest they be ridiculed as “crazy,” with all their views summarily dismissed.

In most cases, this may be the correct strategy to pursue, but if handled properly, an exact opposite approach might sometimes be quite effective…Or as suggested in a quote widely misattributed to Stalin, “Quantity has a quality all its own.”

Suppose it is established that there is a reasonable likelihood that the media completely missed and ignored an important matter that should have been investigated and reported. The impact is not necessarily substantial, and many individuals stubbornly wedded to a belief in their establishment media narratives might even resist admitting the possibility that the media had seriously erred in that particular situation.

However, suppose instead that several dozen such separate examples could be established, each strongly suggesting a serious error or omission on the part of the media. At that point, ideological defenses would crumble and nearly everyone would quietly acknowledge that many, perhaps even most, of the accusations were probably true, producing an enormous credibility gap for the mainstream media. The credibility defenses of the media would have been saturated and overcome…

For example, in the original 2013 American Pravda article I raised over half a dozen enormous media lapses, all of them now universally acknowledged: Enron’s collapse, the Iraq War WMDs, the Madoff Swindle, the Cold War spies, and various others. Having thereby set the stage by presenting this admitted pattern of major failure, demonstrating that a considerable suspension of disbelief was warranted, I then extended the discussion to three or four important additional examples, none of them yet acknowledged, but all of them perfectly plausible. Perhaps as a consequence, the article received reasonably good attention including by elements of the mainstream media itself, who are often willing to acknowledge the errors of their class so long as these are presented persuasively and in a responsible manner.

- American Pravda: Breaching the Media Barrier

Ron Unz • The Unz Review • October 24, 2016 • 2,500 Words

This same sort of reasoning also applies to financial matters.

If our markets seem to be severely mispricing one enormous risk, there is a natural tendency to dismiss that possibility. But if there appear to be several such looming financial disasters, all of which have been completely ignored by most traders and investors, faith in the wisdom of these latter market makers begins to dissolve.

Undistracted: Capture ...

Check Amazon for Pricing.

Undistracted: Capture ...

Check Amazon for Pricing.

This conclusion is further supported by some major examples from the last few decades.

Consider the disastrous Dotcom Bubble of a quarter century ago and the even more disastrous Mortgage Bubble from a few years later. If the markets—and the “smart money” investors who dominated them—were so totally wrong in both those cases, perhaps they might be making similar mistakes today.

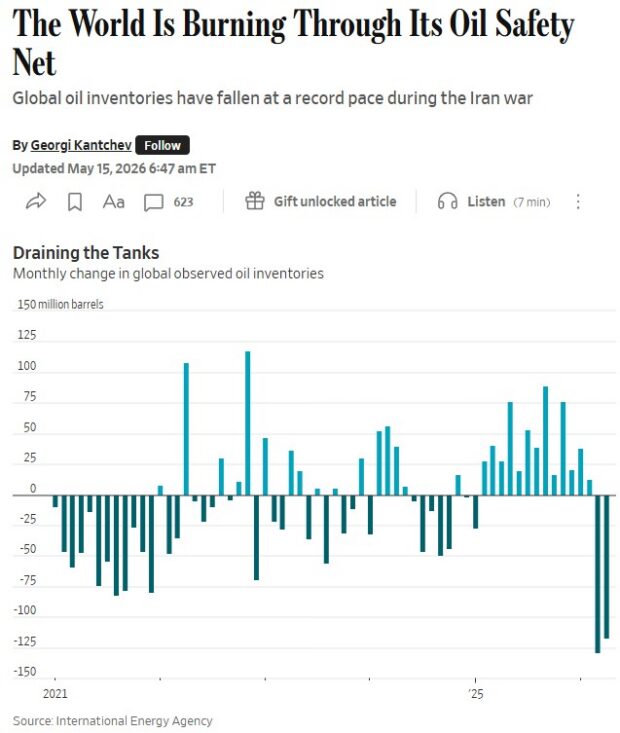

Oil Prices Drop As Oil Supplies Approach “Tank Bottom”

Just over three months ago, America and Israel launched their sudden attack on Iran with a surprise decapitating strike followed by a massive wave of bombardments.

Less than 48 hours later I published my first article on the conflict, and although I discussed many elements, I focused on the Strait of Hormuz as the crucial operational theater.

For decades, the Iranians had threatened to close that vital Persian Gulf waterway if they were attacked, and they had done that. So despite all their heavy losses in leadership and military assets, if they managed to keep it closed against American efforts, they could win the war. A quarter century ago, a famous Pentagon simulation exercise had suggested that the Iranians might succeed, but we were about to test that prospect in real life.

Roughly 20% of global oil shipments passed through the Strait, so if it remained closed, there were widespread expectations that world oil prices would quickly skyrocket to $150 or even $200 a barrel, thereby putting tremendous economic pressure on President Donald Trump and his government to end the conflict.

During the weeks that followed, Trump issued endless loud demands that the Iranians reopen the waterway to oil tankers and other cargo vessels, but despite all his bluster, threats, and bombing attacks, the Iranians held firm. The world suffered the largest oil supply-shock in history, far greater than those that had devastated the global economy during the 1970s. Indeed, the Trump Administration was so fearful of the grave economic crisis that they quickly arranged a gigantic release of some 400 million barrels from the West’s strategic petroleum reserves, and they also lifted sanctions on the already exported but unsold crude of Russia and even Iran itself.

Yet despite this sudden, massive loss of supply, oil prices only rose a relatively modest amount, nothing at all like the huge spike that almost everyone had predicted.

More than three months later the Strait still remains closed to tanker traffic, but oil prices have recently fallen once again. The August future contracts for Brent crude is now down to just $91 per barrel. This is the lowest level since just a few days after the conflict began when most had expected the war to quickly end, leading to the reopening of the waterway. Furthermore, this price is down some 20% from the peak reached about a month ago, with other oil prices following roughly that same trajectory. So the markets are apparently convinced that the global oil crisis is far less serious than most believe it to be.

Under a properly functioning market economy, commodity shortages soon induce price hikes until a combination of reduction in demand and increase in supply has produced a new equilibrium. But despite the loss of perhaps 14M barrels per day of oil, the resulting price rise has been far too small to have had that necessary impact.

Vital Proteins Collage...

Check Amazon for Pricing.

Vital Proteins Collage...

Check Amazon for Pricing.

For example, according to an article in the Economist, higher prices have led to increased oil production in Canada, Venezuela, Norway, and Brazil. But all of these countries combined have only raised their exports by less than 1M barrels per day, hardly impacting the huge global shortfall.

There had been widespread claims that the American frackers would quickly boost their output to compensate for any loss of Persian Gulf oil. But an article in the WSJ reported that they had no intention of doing so, with their production only rising by less than 0.03M barrels per day, a totally insignificant account.

These days oil use is highly inelastic, and according to a recent interview with Prof. Steve Hanke, the relatively small increases in oil prices have only reduced global demand by about 2M barrels per day, a figure that I’ve also seen reported elsewhere.

So due to the minimal rise in global oil prices, the response of market forces to the large and continuing shortfall in Persian Gulf oil has been completely inadequate on both the supply and the demand sides of the equation. As a result, the world seems heading towards what might be called “a very hard landing.”

A couple of weeks ago, a major article in the Wall Street Journal emphasized that the existing oil stockpiles that have been cushioning our current shortfall were rapidly being exhausted.

Drawing upon all the figures separately reported in media outlets such as the Journal and the Economist, I had attempted to project when existing stockpiles would be exhausted and the absolute physical shortage of oil would suddenly produce a dramatic spike in prices. I lack expertise in these matters and my estimate of the month of May turned out to be mistaken. But others with far greater knowledge of the industry have continued to issue dire warnings.

On Friday, CNBC reported the alarming remarks of a top oil industry executive:

Exxon Mobil warned Thursday that oil inventories will fall to record low levels in coming weeks, forcing prices to spike and curbing demand.

Nordic Naturals Ultima...

Buy New $32.49 ($0.36 / Count)

(as of 04:49 UTC - Details)

Nordic Naturals Ultima...

Buy New $32.49 ($0.36 / Count)

(as of 04:49 UTC - Details)

“We’re approaching unheard of inventory levels,” said Exxon Senior Vice President Neil Chapman at a conference hosted by Bernstein in New York.

“I mean really, really low levels,” Chapman warned. “You can debate whether that’s going to hit, those really low levels, in two weeks or three weeks. Once you get to that point, then you’ll see price shoot up.”

The price of physical Brent oil cargoes will spike to $150 to $160 per barrel when inventories hit all-time lows in coming weeks, the executive said. “When the price gets to a certain level, demand destruction brings it back into balance,” he said.

Brent futures for July delivery, the nearest contract, closed under $94 per barrel Thursday as investors once again held out hope for a settlement between the U.S. and Iran that will reopen the Strait of Hormuz.

As that story reported, there appears to be a gigantic gap between July Brent oil futures and projected July Brent oil prices.

I suppose this might be explained by a widespread belief that the Iranians are about to fully reopen the Strait to oil tanker traffic just as Trump has been repeatedly claiming for the last three months. But although I lack any expertise in commodity markets, I do feel extremely skeptical of such a geopolitical development.

Meanwhile, a few days ago the Brookings Institution published an excellent analysis of the global oil situation entitled “The Timing of the Impending Crude Crisis” that came to some important conclusions. One point of confusion has been the tendency to loosely conflate the supplies of crude and refined products so the researchers decided to simplify the issue by focusing entirely on the former.

Just as I had done, they took into account the loss of Persian Gulf shipments, the releases from strategic petroleum reserves, the de-sanctioned Russian and Iranian oil, and various other factors. Their figures for each of these were somewhat different than the ones I’d sometimes seen mentioned in the media, so their calculations were also different and probably more accurate. They conveniently summarized all of their results in a simple chart.

According to their analysis, existing global stockpiles should be exhausted in July, at which point prices would spike to something like $150 per barrel or more for Brent oil, just as the Exxon executive had suggested.

This timeline also seemed roughly the same as the one sketched out at the beginning of May by commodities expert Jeff Currie, a senior advisor to the Carlyle Group.

“I’ve never seen anything like it before.”

Storage tanks for oil, jet fuel, diesel, gasoline will be running out in Europe in May.

Oil storage tanks in the United States will run empty “somewhere in the July 4 period,”

– Carlyle’s Jeff Currie pic.twitter.com/TIsL6rKUWX

— Wall Street Mav (@WallStreetMav) May 6, 2026

This supply scenario might be affected if Iran suddenly reopened the Strait of Hormuz. But that would require a capitulation either by the Iranians or by Trump, neither of which seemed very likely to me. So if we excluded those two possibilities, the current future price of $91 for August Brent oil was just as absurd as I’ve been saying all along.

Vital Proteins Collage...

Check Amazon for Pricing.

Vital Proteins Collage...

Check Amazon for Pricing.

One important point was that the Brookings analysis never considered the substantial risk that Trump would choose to restart the war with Iran by attacking that country’s infrastructure. The Iranians have repeatedly warned that if that happened, they would respond with massive force, destroying the energy and civilian infrastructure of the Gulf Arab states that had enabled those attacks. Those exchanges would destroy most of the Persian Gulf oil facilities, drastically reducing supplies for years to come. So under that dire scenario, oil prices would surely skyrocket far past the high levels already suggested.

The contrary factor has been the widespread belief that global oil prices would plummet once a peace agreement with Iran led to the reopening of the waterway, and that such an agreement is now close at hand. This has been the regular refrain of Trump Administration officials including National Economic Council Director Kevin Hassett, who emphasized this point in a FoxNews interview about a week ago.

NEC Director Kevin Hassett: “We’re already seeing signs that people are a little bit wary about buying oil on the spot market right now because they expect the price to drop a lot sometime soon, so that’s a very, very good sign.” – Fox pic.twitter.com/rC2KZioEok

— Energy Headline News (@OilHeadlineNews) May 24, 2026

But a few days later an experienced energy consultant named Art Berman was interviewed for an hour, and he debunked and ridiculed that sort of analysis as absurdly naive wishful thinking.

Drawing upon his half-century of work in oil markets, Berman argued that these sorts of statements by Hassett and others demonstrated their total ignorance of the practical details of the oil industry.

Resilia Softgels with ...

Check Amazon for Pricing.

Resilia Softgels with ...

Check Amazon for Pricing.

Even once the Iranians fully reopened the Strait to traffic, it would probably take several months before the huge number of trapped tankers could exit the Persian Gulf and reach their various global destinations, so the massive shortage of oil supplies that would be hitting the world in July was already baked into the cake. Under the best of circumstances, the severe shortages would continue at least into September, and Berman even believed that tanker traffic would remain less than half of its previous levels for a year or more after any such reopening.

THORNE Creatine - Micr...

Check Amazon for Pricing.

THORNE Creatine - Micr...

Check Amazon for Pricing.

Sports Researchu00ae O...

Check Amazon for Pricing.

Sports Researchu00ae O...

Check Amazon for Pricing.

NatureWise Vitamin D3 ...

Buy New $14.99 ($0.04 / Count)

(as of 11:50 UTC - Details)

NatureWise Vitamin D3 ...

Buy New $14.99 ($0.04 / Count)

(as of 11:50 UTC - Details)

Sports Researchu00ae V...

Check Amazon for Pricing.

Sports Researchu00ae V...

Check Amazon for Pricing.

Copyright © The Unz Review

The Federal Reserve Is Why the People Are Unhappy

The Federal Reserve Is Why the People Are Unhappy