Sarajevo Redux or How World Wars Come About

And the relevance to Israel, Gaza, and the wider Middle East.

February 6, 2024

On 28 June 1914, Archduke Franz Ferdinand and his wife Sophie were assassinated in Sarajevo. Who would know that in only a few weeks the whole of Europe would be at war, leading to the deaths of millions. Are we facing a similar escalation of events today?

Nowadays, we would ascribe runaway events like these to chaos theory, but it wasn’t so in 1914. They were sequenced with the principal actors seemingly unable to stop them. Austria-Hungary called in Germany and together they declared war on Serbia. That brought in Russia, Serbia’s ally, so Germany declared war on Russia. Russia’s ally, France, mobilised her forces so Germany declared war on France, bringing in Britain which declared war on Germany on 4 August. In a little over five weeks from the Sarajevo assassination, all the European combatants had embarked on the most destructive war in all history. It came out of nowhere and was to last over four years.

The War on Terror: The...

Best Price: $10.25

Buy New $14.99

(as of 12:25 UTC - Details)

The War on Terror: The...

Best Price: $10.25

Buy New $14.99

(as of 12:25 UTC - Details)

Central to the escalation was one nation — Germany. Central to the current Middle East crisis is one nation — The United States.

Today, we could be in the early stages of a similar escalation of events triggered by Israeli attempts to eliminate Hamas in Gaza. So far, the progression of events has been subdued, notably to some activity by the Houthis at the Bab El-Mandeb Strait disrupting shipping. Predictably, this is proving difficult and expensive to deal with and shows signs of leading to more intensive attacks by NATO participants on Yemen’s Houthis. But the Houthis are allied with Iran, and Iran supports both Hamas and Hezbollah. Iran is now allied to Russia which is winning the war against NATO in Ukraine. And Russia is allied with China which is claiming Taiwan. It is beginning to rhyme with Sarajevo all over again, but on a global, as opposed to a European scale.

The escalation into a new world war could have further to go than previously, with nuclear weapons in the armouries of most of the combatants. Surely, it would be complacent to think that they will remain as an unused umbrella, never to be deployed. But we can see how developments considered only one step at a time can take us to a very dark place.

Additionally, there is a currency angle today. The First World War was not about currencies, but today the Americans find themselves having to protect their dollar’s hegemony and credibility, something that was not an issue when gold was the money to which all currencies individually referred.

With the United States’ finances already in a perilous state, to embark on a new world war would most likely undermine the dollar’s value and credibility as a currency, achieving one of the Asian hegemons’ objectives at a stroke. The rest of the neutral world outside the narrow western alliance will watch this with interest because many of them owe dollars and presumably would happily see it devalued.

Last week, we saw senior military sources in Britain warn that in the circumstances Britain’s armed forces are insufficient to deal with the potential threat from Russia and that military conscription would have to be considered. Was this just lobbying for more funds by the Ministry of Defence as it periodically does, or was it part of a CIA/MI6 campaign to prepare us for war? Bearing in mind that the US uses NATO to prevent having to call up her own citizens and that the UK Government when asked by the US to jump merely asks how high, then perhaps this call to arms should be taken seriously as an indication that the intelligence services believe that events are leading towards a third world war.

This article examines the political interests likely to decide the direction of the crisis centred on Israel. By its actions, the Israeli government betrays a deep sense of insecurity — as well it might. The shift in the Middle East’s tectonic plates started with Mohammed bin Salman’s 2017 purge of corrupt Saudi businessmen and dignitaries, which effectively reduced American influence over the Kingdom. This was because America’s foreign policy has always been carrot or stick: to buy influence or threaten adverse consequences.

By side-lining US bought influence in Saudi Arabia, MBS’s dramatic action will have left Israel feeling isolated and vulnerable. And by MBS removing US control over Saudi Arabia, US wider command over the whole region was compromised. This became increasingly obvious as the Saudis’ diplomatic relations were restored last year with Iran as part of a wider unification of the Muslim nations in the region. US divide and rule policies isolating Iran had become redundant. And finally, the Saudis killing off the petrodollar monopoly and turning to the Asian hegemons and the petroyuan was a significant blow to Israel’s only real friend.

The sense of insecurity in Israel must have become acute. Realistically, there were only two policy options for her government: work extremely hard towards restoring trust and keeping relations with her Muslim neighbours on an even keel, with a view to working with all of them towards the political integration of Palestinians in Israel and providing credible guarantees for their security. Or alternatively, act aggressively to remove the Palestinian problem entirely. Anything in between would almost certainly fail. Given its political constituency, Netanyahu’s Likud party chose the latter option, only taking a belated decision on Gaza after Hamas’s October excursion killed Israelis and took hostages.

The die was cast, uniting the world’s two billion Muslims in opposition. The feeling of isolation in Jerusalem must now be acute, with Hezbollah and other enemies well equipped by Iran. Israel is now fighting a proxy war with Iran through these organisations. In order to survive, Israel must not only maintain unconditional support from America, but to push America into confronting Iran either to the point where Iran agrees not to supply its many crusading proxies and backs off entirely, or America committing to whatever it takes in an all-out conflict against Iran.

Understandably, without Saudi support America is reluctant to be drawn into this mess, but it is hard to see how it can be avoided. Israel is not now in a position to back down without a change of government leading to appeasement, and there’s no time for that even if it was possible. If anything, the threat to Israel’s very existence is increasing, and it is difficult to see how she can survive without a full military commitment from America. Unless, of course, she deploys her own nuclear arsenal which can only lead to mutual destruction.

We shall start with Iran. The hate against Israel has been indoctrinated into the various Iran-backed militias: Houthis, Hezbollah, the Islamic Resistance in Iraq (including Harakat Hezbollah al-Nujaba), and Iraq’s Popular Mobilisation Forces, along with sites in Syria belonging to the Iranian Revolutionary Guard. Imbued with religious-based hate against Israel, they are not operationally under the control of Tehran and so are potential wild cards.

It would be a mistake to view Tehran itself as comprised entirely of extremist mullahs, when there are some shrewd diplomats directing policy. Iran became a member of the Shanghai Cooperation Organisation last July, has an important role in the industrialisation of Middle Asia, and works closely with Russia on energy policies. Ultimately, Putin and Xi may be described as the master strategists pulling Iran’s strings in the background.

Putin and Xi are well-versed in war tactics. Russia has a history of letting its enemies extend themselves beyond their support lines (cf. Napoleon, Hitler) and China has the wisdom of Sun Tzu on warfare. Some Sun Tzu pearls: “All warfare is based on deception”, “Hold out baits to entice the enemy” (Houthis, Hezbollah ect.), “If your opponent is of choleric temper, seek to irritate him. Pretend to be weak, that he may grow arrogant.” Doesn’t this last one just describe the US’s political class?

Iran’s new strength is not just in its greater Asian alliances, but the new ones with the Saudis and other members of the Gulf Cooperation Council. Iran’s skilled diplomats will be sure to keep their new Arab friends onside in the interests of common objectives with respect to oil policies. Iran will avoid direct confrontation with the Americans and Israelis, as much as possible.

The signals sent by European and American climate change policies calling an end to fossil fuels were bound to drive Middle Eastern energy exporters eastwards into Asian markets, which also happen to be where oil and gas demand is rising more rapidly. It is a trend which had even been reflected in the recasting of gold bars from LBMA to Chinese standards, observed in Swiss refiners ten years ago. Logically, the political alliances began to reflect the economic interests and with Russia being the largest exporter of oil and gas (the Saudis are the largest exporters of oil only) there was a cartel aspect as well.

Together with the reproachment between the Saudis and Iran, this has changed the geopolitics of oil with respect to Hormuz. In the past, there was always the threat that an American attack would lead to the Straits being closed by Iran. But now, closure of Hormuz would inflict damage on China and India who are fellow members with Iran of the Shanghai Cooperation Organisation. For that reason, the disruption of supplies to Europe is better executed at the Bab El-Mandeb Strait by the Houthis, who are selecting which shipping is allowed through. Chinese and Russian vessels have free passage, while those owned, flagged, or having port destinations of Israel and the Houthis’ enemies are in danger of being attacked.

Economist Michael Hudson[i] suggests that for these reasons America might somehow close the Hormuz Strait with a view to cutting off supplies to Asia, America being self-sufficient in oil, and her trade supplies being delivered across the Pacific anyway. Hudson suggests that that would give oil price control back to the US, but he fails to mention the benefit to Russia, and that the oil price shock would destabilise financial markets with catastrophic consequences for the dollar-based credit system.

Dangerous Liaison: The...

Check Amazon for Pricing.

Dangerous Liaison: The...

Check Amazon for Pricing.

I think we can rule that out. Realistically, until events otherwise determine the Arabs will sit on their hands, without intervening, Knowing that it is America which has the problem, nothing is to be gained by taking sides. The Houthis, Hezbollah and other Islamic factions will presumably continue to harass Israel, and Iran will probably continue to supply them. The exception perhaps is that along with Iran, Iraq will continue to push for the Americans to close their bases and remove their 2,000 personnel.

Meanwhile, the dangers to Israel’s continuing existence will continue, bringing more pressure from Israel for America to attack Iran.

As well as the enormous pressure the Jewish lobby brings to bear on the Biden administration, already Republican politicians are in kick-ass mode. In the last of many drone attacks which have so far gone without much notice, the death of three military reservists at a border site in Jordan this week has electrified the political scene. In an election year, the pressure on the Biden administration not to look weak is bound to drive policy. All politicians are slaves to the headlines, and a response is now planned. The administration is said to be considering how to strike back without escalating the situation. It’s likely to involve hitting Iran’s proxies rather than Iran and trying to judge how to do so without provoking Iran into a military response.

In this presidential election year, US foreign policy also faces defeat in Ukraine. There is bound to be pressure to cover this up by ensuring the headlines are all about something else, an ill wind which makes the Middle East convenient cover. Whether that will encourage yet more provocation and military support for Israel remains to be seen. But while it would be a mistake to play down dangers of military escalation, equally it would be a mistake to ignore the consequences for inflation, financial assets, and the dollar.

Apart from its military build-up so eloquently forewarned by Erskine Childers’ The Riddle of the Sands, in 1914 Germany declared its European wars from a position of relative financial strength. Today, America has a fiat dollar, a debt to GDP ratio of about 125%, and is mired in a deepening debt trap. It is simply not in a position to embark on an open-ended commitment to support Israel in a war against Iran.

Increasing tensions in the Middle East are likely to drive oil prices higher. Trade disruption will spread, inevitably leading to product shortages, particularly in Europe. Hope that the prospects for global price inflation are diminishing will be dispelled and therefore so will the prospects for a decline in interest rates. Bond yields are already showing signs of going no lower and as they head higher, the threat to financial assets and their collateral values is that they will enter bear markets.

US economic prospects are already dire, with the only growth being in the US budget deficit. Strip out a budget deficit likely to be $3 trillion this fiscal year, add in the consequences for currency debasement and you can see that the US economy is not only in trouble, but markets faces further dilution of the dollar’s purchasing power and therefore rising interest rates and bond yields.

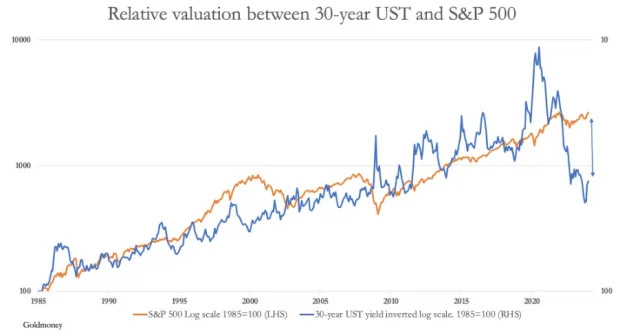

The chart above shows the valuation gap which has opened up between the long bond yield (inverted) and the S&P 500 Index. If the situation in the Middle East deteriorates, it is a recipe for an overvalued equity market to crash.

Even without the Middle Eastern situation deteriorating, the US equity market faces a prospective bear market of significant proportions. The consequences of an escalation will almost certainly trigger widespread reassessments of market risk, and for foreigners owning dollars some fundamental issues will need to be addressed.

That the dollar is simply credit, whose value is based upon faith and nothing else is widely ignored and the implications not understood. But with Russia and China planning to remove the dollar as much as possible from their spheres of influence, in the long run the dollar’s status as the reserve currency is a dead duck anyway. Therefore, there can be little doubt that if America gets drawn into a new Middle Eastern war the dollar’s credibility will be challenged sooner than if events were left to take their course.

The global ubiquity of the inflation and interest rate problem will mean that the values of all forms of credit, including other currencies, are likely to be undermined. This is bound to lead to the price of gold, which is true legal international money without counterparty risk rising expressed in depreciating credit.

The growing likelihood is that a new war spreading in the manner of a Sarajevo redux will crash credit values, including and particularly the purchasing power of dollars. Either this prospect will put off the US’s deep state from pursuing such a course, or alternatively financial markets will have to be shut down for the duration. We have never seen a near bankrupt modern nation with a fiat currency, widely owned often for pure speculation, attempt such a hazardous venture before — nor are we likely to do so again.

Other than a degeneration into a nuclear conflict, this leaves us with only one possible outcome: the US backs off in this stupendous game of chicken and seeks some sort of face-saving exit from Ukraine. For Russia and Iran, it will be the ultimate victory. The dollar’s hegemony will be compromised, so will continue to decline in its value anyway, but at a less catastrophic rate than in a full-on conflict.

Either way, holding credit as opposed to real money without counterparty risk will be the mistake commonly made, and when the wider population begins to understand that this is so, there will be insufficient gold to meet the likely demand at any price.

[i] See https://globalsouth.co/2024/01/21/michael-hudson-on-russia-iran-and-the-red-sea-natos-war-economy-collapses/

Copyright © Alasdair Macleod

From Crisis to Confiscation—Where Do I Store My Wealth?

From Crisis to Confiscation—Where Do I Store My Wealth?