The Bell Tolls for Fiat

July 14, 2023

The importance of Russia’s announcement that a new gold-backed trade currency is on the BRICS meeting agenda for August 22—24 in Johannesburg seems to have gone completely over everyone’s heads, with mainstream media not even reporting it.

This is a mistake. China and Russia know that if they are to succeed in removing the dollar from their sphere of influence, they have to come up with a better alternative. They also know they have to consolidate their trade partners into a formidable bloc, so plans are afoot to consolidate BRICS, the Shanghai Cooperation Organisation, and the Eurasian Economic Union along with those nations who wish to join in. It will be a super-group embracing most of Asia (including the Middle East), Africa, and Latin America.

The groundwork for the new currency has been laid by Sergei Glazyev and is considerably more advanced than generally realised.

This article explains why Russia and China are now prepared to fully back Glazyev’s expanded project. For Russia, it is also now imperative to destabilise the dollar as a deliberate escalation of the financial war against America and NATO. China’s priority is no longer to protect her export trade, but to ensure that her African and Latin American suppliers are not destabilised by higher dollar interest rates.

Introduction

“The BRICS’s introduction of a gold-backed currency, which is supported by 41 countries with large and influential economies, will weaken the dollar and the euro and will benefit countries such as Iran, while Iranians in possession of gold will experience a wealth increase,” Mousavi added [the head of the South Asia Department at Iran’s Foreign Ministry]. The Russian government confirmed a day earlier that Brazil, Russia, India, China, and South Africa would introduce a new trading currency backed by gold.

Iran’s MEHR News Agency[i]

The quote above encapsulates why a new gold-backed currency is desired: it will undermine fiat currencies which have been no friends to oil producers and benefit individuals who own gold making it popular on the streets. RT, the Russian government-financed English broadcasting service had confirmed on last Friday the intention to introduce a new gold-backed currency for BRICS members. The announcement was completely missed by mainstream media, partly because RT and other Russian news sources are censored in many countries in Europe including the UK, and any news out of Russia is disbelieved anyway.

Reactions from those who saw it, even among gold bugs, vary from the opinion that neither China nor Russia could make a gold backed currency stick, to it taking years in the planning and implementation so is irrelevant to today’s markets. But there are good reasons to believe that this complacency will turn out to be wrong, and that events are likely to evolve considerably more rapidly than expected.

The problem for capital markets is that they are dominated by Keynesians, automatically programmed to believe gold is bad and fiat is good. As a stockbroker in London, when President Nixon suspended the Bretton Woods Agreement, I recall there was a similar level of confusion over those implications. And now, 52 years after putting the world on a fiat dollar standard, the majority of the world has had enough of dollar hegemony, has found safety in numbers, and is going back onto a gold standard. Like all life, the pure fiat era is ephemeral after all, defined by its birth and death. Macroeconomics will have to be rewritten.

The move away from fiat has been evolving for a considerable time, with de-dollarisation the ultimate objective of the Asian hegemons. Those tracking developments in gold bullion markets in recent decades have noted the drift of bullion from west to east, and the rise in gold mine output in China and more recently in Russia. Central banks, predominantly in Asia, have been accumulating bullion reserves and adding to declared and undeclared state funds in record quantities. Ultimately, this activity can only be to use gold to secure currency values as the dollar dies or is done away with.

A sudden turn of events occurred when the western alliance imposed sanctions against Russia following her attack on Ukraine. They set off a train of actions that has unified Asia and many of its supplier nations into a rebellion against American hegemony, stoked up by Putin and led by Saudi Arabia and the Gulf Cooperation Council. And since the western alliance turned its back on fossil fuels, the low-cost producers throughout Asia have banded together representing nearly half global oil output, and a third of natural gas. As a cartel, OPEC is now just an appendix to the Asian mega-energy producers.

The new cartel is dominated by President Putin, whose degree from Leningrad University was in energy economics and well qualified to be energy ringmaster. Not only has he demonstrated an understanding of the importance of controlling global energy supplies, but he also has a clear understanding of the importance of monetary gold.

Since the western alliance’s sanctions, the signals coming out of Moscow have been clear: Sergei Glazyev, who is Putin’s point-man for macroeconomic policy has been waving the gold flag since then in plain sight. As a board member of the Eurasian Economic Union Commission (EAEU) since 2019, he was tasked by Putin to design a trade settlement currency for the EAEU. The initial statement through a news agency in Bishkek in early March 2022 reported that it was to be based on the currencies of the member states and a basket of undefined commodities. According to Glazyev, his brief was to create a Eurasian monetary and financial system to the exclusion of foreign currencies, particularly the dollar and euro.

The intention was also to remove exchange controls for cross- border settlements within the Eurasian membership, replacing the dollar as the commonly used settlement medium between them. A week later, in an article for Goldmoney[ii] I concluded that as stated the new currency would not work, and the only logical solution was to do away with the currency basket proposal and use gold backing solely to represent commodities. That way, it would be easy for other nations in the Shanghai Cooperation Organisation (SCO) to join in, which was the ultimate objective from the outset.

In July 2022, Glazyev was behind a move to beef up the Moscow gold exchange, the official line being that having been sanctioned from the London market Russian miners needed a more effective local market. But working in conjunction with the Shanghai Gold Exchange this was an important signal about the way Galzyev’s monetary thinking was developing. Confirmation came on 27 December last year, when he wrote an article for Vedomosti, a Moscow business paper, describing why the rouble needed to return to a gold standard. That article was co-written by his deputy on the EAEU committee designing the new trade currency and was a thinly veiled indication of the committee’s view.

Therefore, you did not have to be particularly astute to discern the trail of clues presented to us. We could assume with justification that gold was intended to be the sheet-anchor for this new currency probably from the outset, but some political hoops had to be jumped through to convince the EAEU member states that it was the solution.

The impracticality of basing a new trade currency on anything else other than gold had been established. It now turns out that this project is almost certainly a Trojan horse for something far larger. It was obvious that other members of the Shanghai Cooperation Organisation should be able to join in, and now it turns out that the invitation is being extended to members of the BRICS club as well. But that’s not all. The entire membership of the SCO, its dialog partners, and associate members will be attending the BRICS conference in Johannesburg on 22—24 August. I am assuming that the original list of 36 nations, which according to most recent reports has expanded to 41, includes the members of the EAEU who were not on the original list — at the time of writing this is yet to be confirmed.

That being the case, the BRICS currency project is not a cold start and not something to be planned for a distant future. The groundwork has already been prepared by Glazyev and the structure can be rapidly assembled once the necessary resolution is adopted. It is even possible that the necessary institution(s) exist waiting to be deployed.

It is also beginning to look like there will be another proposal on the Johannesburg agenda, to merge the SCO, the EAEU and BRICS into a supersized trading block. In terms of both combined population and GDP on a purchasing power parity basis, it is already in excess of half the world, dwarfing the western alliance which kowtows to America.

The US Treasury would almost certainly have known about the BRIC proposals when the agenda was first circulated, which probably explains why at short notice Janet Yellen, US Treasury Secretary flew to Beijing. From her department’s point of view, if the new currency proposal was to be adopted its financing of the budget deficit would be adversely affected, not to mention the threat to the dollar’s hegemony. The principal card up her sleeve was to threaten greater sanctions against China’s exports, not just to America, but to her allies as well, but we don’t know if it was actually discussed in these terms.

The Chinese view

For too long and too often China has been threatened over access to markets by the Americans. We can be sure that ahead of the BRICS currency proposal the Chinese have gamed this possible threat being acted upon and come up with their own conclusions about its economic consequences. Russia’s experience, which harmed the sanctioning countries considerably more than the sanctioned, will have been fed into these calculations. One suspects that other than signalling to the Chinese and Russians that there is an increasing level of alarm in Washington, Yellen’s mission will have achieved little. And an important factor for the Chinese attitude is their experience of the US’s attempts to destabilise Hong Kong, which led to it being taken directly under Beijing’s control. It is therefore important to understand China’s analysis of America’s objectives and methods in order to define her own position.

In April 2015, Qiao Liang, the People’s Liberation Army Major-General in charge of intelligence strategy gave a speech at a book study forum of the Chinese Communist Party’s Central Committee.[iii] Qiao commenced by stating the obvious, that the U.S. enforces the dollar as the global currency to preserve its hegemony over the world. And he concluded that the U.S. would try everything, including war, to maintain the dollar’s dominance in global trading. But what he then went on to say is extremely relevant to the current situation. He described US’s actions with respect to foreign national debts.

Qiao made the case that both the Latin American crisis in 1978—1982, and the Asian crisis in 1996—1998 were engineered by America. By reducing dollar interest rates to below their natural level they would weaken the dollar and encourage an investment boom in the targeted jurisdictions, funded by dollar credit. They then increased interest rates and strengthened the dollar to create a financial crisis. These events did, indeed, happen, but perhaps driven by the cycle of bank credit, as much as by foreign policy.

The relevance of Qiao’s analysis is that today, the same conditions appear to be targeted not against China, which does not borrow dollars, but at the dollar indebted nations around the world with which China trades — the BRICS nations. Informed by Qiao’s analysis, it must appear to China that America’s persistent strategy is to continue to raise interest rates even after the inflation dragon is slain, and by bankrupting them the US will attempt to bring the nations seeking to join BRICS back under her control.

That being the case, China will have weighed up the consequences for her export trade against the likely sanctions America and her allies could threaten and decided that the real threat is against the emerging economies in Africa, Latin America, and elsewhere which have received substantial Chinese investment. In financial terms, it is therefore imperative that this threat be addressed in a pre-emptive attack on the dollar, which can only be achieved by exposing the dollar’s weakness as a fiat currency. At least since the Lehman crisis, China and more recently Russia have had the power to do this.

Furthermore, the New Development Bank, which is headquartered in Shanghai, will be able to provide credit either in yuan or the new BRICS currency at lower interest rates to offset the undoubted strains imposed on BRICS members as a result of rising US interest rates. Therefore, China is fully prepared to counter what General Qiao Liang described as the American strategy of “harvesting” assets in foreign countries.

It is important to understand what China believes and motivates her, not whether Qiao is right or wrong. But given that his view is inculcated in the Chinese government, China is ready with Russia to mount an attack on America’s fiat currency by returning to a gold standard for trade, and ultimately for their own currencies.

The Russian view

It should be clear that the current plans for a trade currency originated in Russia, and not China. Indeed, until now China will have been reluctant to destabilise the currencies of the western alliance, because of her export interests. But not only has the relationship with America deteriorated over Taiwan, not only is it clear (in China’s view) that America plans to bankrupt the BRICS members and all those seeking to migrate away from the dollar’s hegemony by raising interest rates, but it is now also clear that neither Russia nor America can back down over Ukraine. Consequently, unless China and Russia together take the initiative, shortly Russia will be directly at war with America and her NATO allies and China will almost certainly be dragged into the conflict over Taiwan. World War 3 must be forestalled.

It is clear that NATO, under the thumb of America, is determined to defeat Russia, remove Putin, and gain control of its massive natural resources. The proxy war being fought in the Ukraine appears to be failing with Zelensky’s summer offensive having ground to a halt. And following the Wagner debacle, Russia is now in a strong position to counterattack. This has led to President Biden being prepared to send the Ukrainians cluster bombs, increasing the urgency for a Russian counter-offensive.

Furthermore, with Ukraine’s summer offensive failing, NATO’s theatre of operational strategy is moving to Poland and the Baltics (Biden was in Vilnius this week for a NATO summit), with Poland particularly becoming a client state of America through NATO. The build-up of military personnel and missiles in Poland will become increasingly obvious in the coming weeks and is already anticipated by Moscow. We await Putin’s reaction, but he is unlikely to just sit on his hands and let NATO build its forces in Poland and the Baltics.

Compromise is out of the question, because it is plain to Putin that America cannot back down. Imagine the consequences for Biden, who started his presidency with the withdrawal from Afghanistan if he ends it with a withdrawal from Eastern Europe. Furthermore, the neo-cons are firmly in charge of policy, determined to defeat Putin, add Russian territory to their sphere of influence, and leave China isolated.

Putin’s terms for peace would be unacceptable to America because he insists on protecting Russia’s borders, which means that all missiles and American bases be removed from Eastern and Central Europe. For Moscow, this raises the question as to whether Russia should simply secure its current position or take Ukraine, which can then be set up as a buffer state. A Russian attack is bound to drive up energy, cereal, and fertiliser prices, worsening price inflation in western alliance countries and causing division with America and Britain, but to the benefit of Russia’s finances which are coming under pressure. Additionally, a successful attack on their currencies’ credibility would undermine the alliance’s military capability, so the dollar should be attacked financially as well.

No one can be sure whether destroying the dollar would avert a nuclear war, but there is little doubt that so long as America can finance its aggression that events are drifting in that direction. From Putin’s viewpoint, undermining the dollar must now be a priority, perhaps combining it with taking Kiev now that Zelensky’s summer thrust has failed.

An advantage of a financial war is that it need not be declared, therefore there is no official victor, and no need for a post-war reconciliation.

Designing a gold-backed trade currency

A new trade currency has the advantage that it will not ever be used as a means of funding government deficits. And given that its role is limited to cross-border trade settlement and and dealing in physical commodities it has to be institutionally acceptable and does not have to appeal to public confidence. Much of the credit will be self-extinguishing. It is additional to national currencies, leaving individual nations to manage their own currency policies, which is why such a currency can enjoy widespread support. It is not to be used as a medium for capital investment.

As the groundwork appears to have been already established by Sergei Glazyev, it could be ready to use as soon as it is approved in August. Besides a strict and simple set of rules, all it needs are two things: the establishment of an issuing entity, and physical gold. The first can be done in a flash, if it is not already established, and the gold will be allocated from the reserves of participating central banks. This is almost certainly why central banks of many of the putative membership of BRICS have been adding bullion to their reserves. They must be extremely thankful for actors in the western financial establishment who trade paper gold in ignorance of this outcome.

The bulleted list that follows is a brief outline of how a new trade settlement currency based on gold can be quickly established to replace the fiat dollar in all transactions between member nations, updated from an earlier Goldmoney article on this topic.[iv] It will be interesting to see how its elements compare with Glazyev’s proposition.

It is designed to be politically acceptable to all involved, as well as a long-term practical solution to facilitate the Russian Chinese axis’s ambitions for an Asian industrial revolution, encompassing Africa and Latin America, free from interference by America and her allies. The essential elements are as follows:

- The announcement of the creation of a new issuing central bank (NICB, not to be confused with the existing New Central Bank in Shanghai, whole purpose is to fund investment in the BRICS members) and a new gold-based currency on the lines below is the first step.

- The NICB is established with the sole function of issuing a new digital currency backed by physical gold. It will be designed to be a fully trusted gold substitute, independent of existing fiat currency values.

- The new currency will only be redeemable for gold between the NICB and participating central banks. They will be free also to add to their NICB currency reserves by submitting additional gold to the NICB at any time.

- The NICB’s eligible participants will be the central banks of participating nations, broadly limited to member nations, associates, and dialog partners of the EAEU, SCO, and BRICS, and additionally nations applying for membership of any of these organisations on an approved list.

- The NICB’s currency is issued to approved national central banks against their provision of a minimum 40% gold backing for it. For example, currency representing one million gold grammes secures an allocation of 2,500,000 currency units denominated in gold grammes. The gold does not have to be delivered to a central storage point but can be earmarked[v] from within a central bank’s gold reserves, on condition that it is securely stored in vaults on a list approved by the NICB. This list is likely to exclude gold stored at central banks of the western alliance and must not be leased or swapped.

- A participating central bank records the new currency units allocated to it as an asset on its balance sheet, balanced by an increase in its liabilities as equity. A participating central bank’s balance sheet is thereby strengthened.

- A participating central bank can offer credit and take in deposits tied to the new currency’s value, to and from the commercial banks in in its national network. Note that the new currency is available exclusively to participating central banks, upon which they can base their own credit dealings with commercial banks.

- Commercial banks trading in member nations and elsewhere will be free to create and deal in credit denominated in the NICB’s new currency. They will have no credit relationship with the NICB, but their regulating central bank will.

- Commercial banks whose central bank does not have access to the NICB currency can clear through wholesale credit markets and will be always free to acquire physical gold in the markets, should they wish to back credit created in the new currency with gold itself.

- All taxes and restrictions on gold ownership must be fully rescinded by participating nations, recognising its historic and legal status as money.

- An efficient central clearing system for commercial banks dealing in credit based on the new currency will be established.

- Asian commodity exchanges in the expanded BRICS will price all products in the new NICB currency as well as in dollars. Intra-BRIC imports and exports will similarly be priced. This will ensure that physical markets and their derivatives are insulated from a fiat currency collapse, a likely consequence of gold’s return to its true monetary status.

The purpose of the new currency is to provide the basis for trade finance and other cross border financial settlements on a sound money basis. The expansion of credit based upon it will grow strictly in line with economic activity and therefore will not be inflationary, undermining its purchasing power. Last week, in an article for Goldmoney I explained why when tied convincingly to gold, commercial bank credit grows on a non-inflationary basis when distortions from the lending cycle are removed. This is the key to understanding why a new trade currency constructed on these lines will endure.[vi]

It is also likely to lead to participating nations placing a greater emphasis on their own currencies’ stability while providing a safe haven from the consequences for the dollar following its introduction. Once the new currency is established, it will be in Russia’s interests to put the rouble back on its own gold standard, and China may follow with the renminbi.

All empirical evidence informs us that when gold becomes the means by which credit is valued, credit’s own value becomes tied to that of gold and is not dependent on stability in the quantity of credit. Operating as a gold substitute imparts pricing certainty to trade and investment and leads to stable, low interest rates giving the necessary conditions for maximising economic development in emerging economies.

Constructed on the lines above, it should be simple and quick to establish. It must be free from attack by members of the western alliance trying to preserve their own fiat currency systems. And the 40% gold backing rhymes with the basic requirement for a metallic monetary standard set by Sir Isaac Newton, when he was Master of the Royal Mint.

For participating central banks, the replacement of gold in their reserves for allocations of the new currency would represent a significant increase in their balance sheet equity. As confidence in the scheme builds, it could be argued that only minimal gold reserves need to be retained by participating central banks, with the balance swapped for the new currency. For example, the Reserve Bank of India officially possesses 787.4 tonnes of gold. Converted into the new gold currency, its value in reserves is uplifted to 1,968.5 tonnes equivalent, added to its equity capital.

The impact on gold

Throughout history, money has been gold, and the rest credit. When you detach credit from gold, there are consequences. Pricing goods and services in credit diverges from pricing them in gold. It is really that simple.

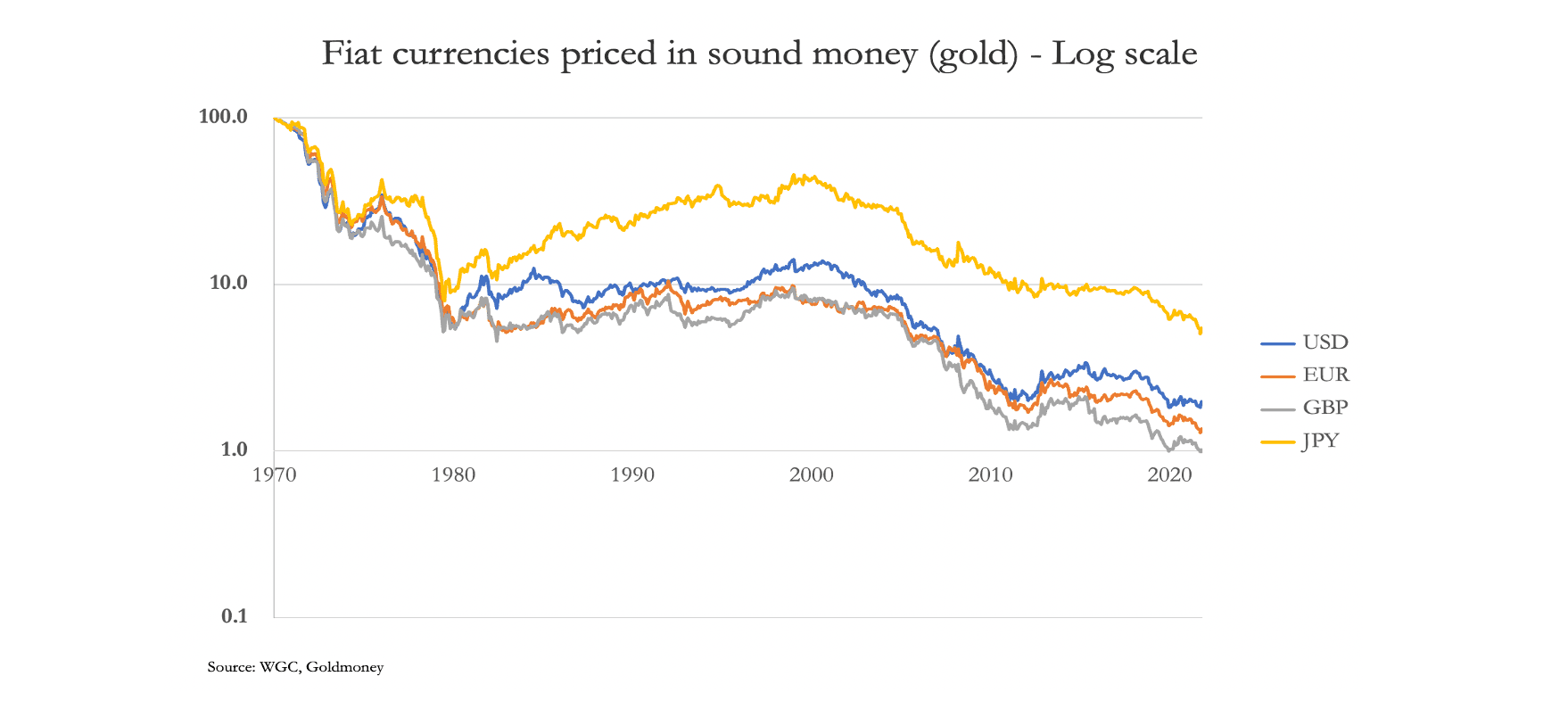

It is widely assumed that fluctuations in prices have nothing to do with the medium of exchange, and for individual transactions it is certainly true that both buyer and seller will share this view. But over time, with official policies aiming for a 2% fall in purchasing power for the dollar and other major currencies it is not true that price fluctuations are entirely due to changes in the demand/supply balance for commodities and other manufacturing inputs. In fact, since the end of Bretton Woods, measured in real money which is gold, the loss of purchasing power has been considerably in excess of the 2% annual target. The chart below puts it directly in a gold versus fiat context.

Since the suspension of Bretton Woods, the dollar has lost 98% of its value relative to gold. The other major fiat currencies have been similarly impoverishing for their users and savers, and only now is the final act in their destruction looming due to the introduction of a new BRICS gold-backed currency.

Through the medium of gold, participating central banks will exchange their reserve dollars for the new NICB currency. Immediately, this rejection of the dollar by a large number of central banks will devalue it further, followed by foreign non-government entities seeking to reduce their exposure. Initially, this will be seen as a run on the dollar into gold, similar to that which followed the suspension of Bretton Woods on 15 August 1971. The market was similarly nonplussed then as it appears to be today, with the London morning fix on Monday 17 August at $43, slightly down on the previous week. It wasn’t until 19 November that the morning fix exceeded $43 again for the first time. It took two whole months for the implications to sink in. But when they did, the price rose to $197.50 on 27 December 1974.

The lesson for us in this Keynesian world is that two months of static prices following the suspension of Bretton Woods is proof that gold was poorly understood in financial markets, and still is today. Derivative markets, particularly the London forward market and Comex futures for the last forty years have lost sight of gold being money and assumed it is a trading counter which plays on irrational fears of instability of the modern currency system. But with the return of gold as the anchor for credit values for the Asian hegemons and their sphere of influence, those fears will suddenly become rational.

The wider consequences of a BRICS currency gold standard

We can assume that the consequences of Asian trade settlements backed with gold will have been carefully considered by the Asian superpowers, particularly by the Russians who have faced weaponised dollars.

Besides bringing stability to export values there are other advantages to reintroducing gold into currency systems. Interest rate stability at lower rates is an obvious benefit. Currently, the Bank of Russia’s key interest rate is 7.5% and price inflation has collapsed to 2.3% (April). The yield on Russia’s 10-year OFZ bond is still 11.3%. If the rouble becomes a credible gold substitute, price inflation, interest rates, and bond yields can be expected to decline and maintain levels that reflect gold’s long-term stability, particularly in more normal times when the Russian government runs decent budget surpluses. And assuming that credit expansion by Russia’s commercial banks is not cyclically excessive, there is no reason to expect otherwise than that financial stability for the currency and the Russian economy would continue in the long-term. Coupled with low taxes (Russia’s income tax is a flat 13%) this stability can be expected foster genuine economic progress and the accumulation of personal wealth for the Russian people. It would be a far better outcome than the current situation and it would secure Putin’s legacy.

However, a move towards gold backing for their currencies by the Asian hegemons can be expected to undermine the purchasing power of western fiat currencies. International capital will abandon ephemeral fiat currencies for real values in commodities, with nations rebuilding stockpiles of energy, metals, and other raw materials instead of accumulating fiat paper. Precious metals, specifically gold, will be sought and its price can be expected to reflect the demise of fiat currencies.

The consequences for wholesale and consumer prices in the western nations would rapidly become obvious, with central banks forced to revise their expectations for price inflation sharply higher. Bond yields can be expected to rise further, undermining all financial and property values. As this negative outlook clarifies, measured against gold fiat currencies will likely enter a substantial relative decline.

The consequences of the emergence of gold backing for currencies in Asia on the currencies and economies of the western alliance are bound to differ in their detail for the currencies in the western alliance.

The reliance on inward foreign investment has protected the dollar from continual trade deficits and played a key role in funding US Government debt since the end of Bretton Woods. It has allowed the US Government to run budget deficits more or less continually. The ending of the fifty-two years of a fiat regime changes all that. The US Government will face significant funding hurdles against foreign liquidation of Treasuries. Bond yields and funding costs for the government are bound to rise significantly.

The consequences for the EU and the eurozone would be both politically and economically divisive. If it were not for political constraints, Germany would naturally drift towards cooperation with the sound money regimes emerging to her east, particularly as the finances of the Mediterranean club deteriorate. With rising bond yields, the entire euro system comprised of the ECB and its national central banks would need to be recapitalised, being already deeply in negative equity. The eurozone’s global systemically important banks (G-SIBs) are extremely highly leveraged and unlikely to survive the combination of falling asset values and bad debts that would be the certain consequences of the euro’s declining purchasing power. Having been assembled at the behest of a political committee and now managed by a political cabal, the euro is at risk of losing all market credibility.

The consequences for the UK pound will also be significant. In a similar debt trap to that of the US Government, the British have the further disadvantage of an economy suffering under increasing taxes. Furthermore, with London being the international financial centre, the UK will be at the epicentre of a fiat currency crisis. For the size of her economy, the UK has little in the way of gold reserves, hampering any future escape from the fiat currency trap.

The major governments aligned both economically and intellectually with the fiat dollar will be left at a comparative disadvantage by a BRICS gold-backed currency, possibly followed by Russia and China adopting gold standards. Interest rates, which are escaping from central bank control, will rise due to two factors: there is the credit crunch from the turn of the bank credit cycle, and the deteriorating outlook for fiat currency purchasing powers. It is the worst of both worlds. Furthermore, economists in governments and central banks would be reluctant to abandon their embedded economic and monetary policies. And will be slow to react.

The only salvation will be for western governments to jettison Keynesian macroeconomics entirely and revert to classical economic theories. The false assumptions that have built up over the fiat currency era will have to be overturned. Crises of this sort nearly always emanate in the foreign exchanges because it is foreign holders of currencies who are the first to recognise a currency’s weakness. Usually, it involves a specific currency. But this time, it will affect all the major currencies in the western alliance.

[i] Official Iranian news release. See https://en.mehrnews.com/news/203015/BRICS-currency-to-benefit-Iran-undermine-US-dollar-euro

[ii] See https://www.goldmoney.com/research/designing-a-new-currency-is-impractical

[iii] See http://chinascope.org/archives/6458

[iv] See https://www.goldmoney.com/research/cbd-cs-the-good-the-bad-the-ugly under the sub-heading, The Good.

[v] Earmarking is the technical term whereby one central bank acts as custodian for another central bank’s bullion.

[vi] See https://www.goldmoney.com/research/the-real-determinants-of-currency-value

Reprinted with permission from Goldmoney.

Copyright © Goldmoney Inc.

Three Important News Items Most of the Media 'Forgot' To Tell You About

Three Important News Items Most of the Media 'Forgot' To Tell You About