Reefer Madness and More

February 12, 2021

We sometimes wonder what they are smoking down on Wall Street, but today the question might better apply to the homegamers who are apparently hitting their bongs down in mom’s basement.

We are referring to Wednesday’s rip-snorting 47% rise in the stock of Tilray – the lead rabbit in the Reddit run on pot stocks.

As it happened, the day that GameStop peaked on January 27th, the once left for dead Tilray was valued at $2.9 billion. Thereafter it went vertical, weighing-in at $10.6 billion upon Wednesday’s close.

That’s not bad, of course, for a company with a mere $201 million of LTM sales, a net loss of $487 million and negative free cash flow of $261 million. And it’s not getting any better, either.

Since going public in 2018, the company’s net loss (blue line) has grown by 60X and its free cash flow (orange line) hemorrhage has worsened by 15X.

Indeed, when you look at Tilray’s three-year history as a publicly traded company, the massive swings in the market cap of this money loosing marvel are about as close to pure reefer madness as you can get without inhaling.

In fact, its market cap has swung by 25-fold over the period:

- July 2018 IPO: $2.7 billion;

- September 19, 2018 peak: $20.0 billion;

- March 19, 2020 swoon: $425 million;

- Year-end 2020 recovery: $1.3 billion:

- Feb 10 Reddit Rip: $10.6 billion;

Tilray Market Cap, 2018-2021

Price discovery?

Perish the thought. The chart above is simply the detritus of drunken speculators high on Fed supplied liquidity, chasing the momentum rabbit from pillar to post and back.

Nor is this mockery of the capital markets merely an outlying instance of irrational exuberance on steroids – an aberration that has no bearing on the larger economic and financial picture.

The Triumph of Politic...

Best Price: $2.56

Buy New $15.99

(as of 05:55 UTC - Details)

The Triumph of Politic...

Best Price: $2.56

Buy New $15.99

(as of 05:55 UTC - Details)

To the contrary, the single most important price in all of capitalism is the price of debt and equity capital: Efficient pricing and allocation of scarce capital is the elixir which makes prosperity go, while its opposite – blind, momentum based gambling – is the ultimate harbinger of malinvestment, waste and stagnation.

Stated differently, getting wasted on Tilray’s product may well add to individual consumer utility and is none of the state’s business, besides. But wasting capital and trading resources in the manner depicted in the chart above is at the heart of what ails the US economy.

That is to say, main street is failing because the central bank has turned Wall Street into a giant, dangerous, wasteful casino that channels both financial and human capital from productive uses into mindless wagering. At length, the resulting capricious windfall gains and losses create social unrest, even as they detract from the business of sustainable growth and wealth creation.

We do reckon, of course, that occasionally a startup of true technological brilliance surrounded by patent-protected moats might initially be worth something like 53X sales during its early years, which is where Tilray closed Wednesday; or even 15X the pro forma revenue it claims will result from its year-end merger with another pot peddler called Aphria.

Still, a commodity dope purveyor which grows the stuff in greenhouses, sells through pharmacies and on-line and has no patents, no barriers to entry and no material brands is another kettle of fish.

The fact is, no matter how many vastly overpriced M&A deals it consummates, Tilray has no hope of dominating a market which is exploding with competitors and startups. That’s owing to the legalization wave now in full force all around the world, on the one hand, and to the endless flood of desperate venture capital, on the other.

So if there were ever a hot new product headed for rapid commodification, cannabis would be it. In that context, it is worth noting that Tilray is also valued at an insane multiple of its commodity output.

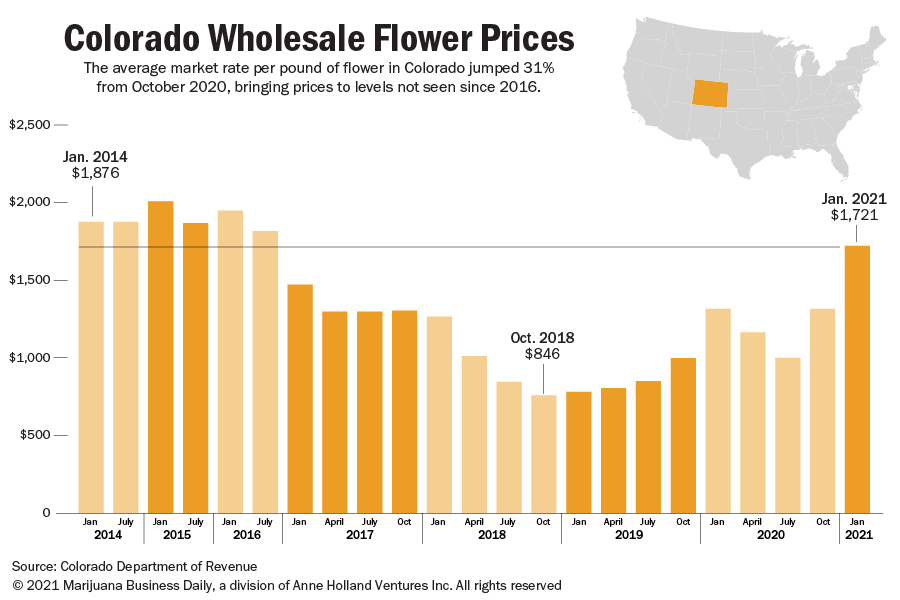

To wit, its average selling price for cannabis flower during 2020 was about $1,700 per pound, and even if you believe its claim of $685 million of pro forma revenue after the Aphria merger, its total output would not exceed 400,000 pounds (actually less because it sells some hemp at higher prices).

So at today’s closing price the company was valued at a minimum of $25,000 per pound of weed sold.

So let’s see. Being a resident of the enlightened state of Colorado, your editor has some acquaintance with the going prices for the product at hand. As shown below, the average price most recently was about $1,700 per pound, but at that level Tilray makes just $200 per pound of gross profit before its considerable overhead and marketing costs.

So the raging robo machines and Reddit crowd today managed to value Tilray at 133X its pro forma gross profit!

But that ain’t the half of it. As Forbes magazine recently put it, once the legal barriers in the US and Canada are removed entirely, cannabis farming will end up on the same competitive ground as corn, soybeans, lentils and lettuce – meaning that current wholesale prices will come tumbling down.

The Great Deformation:...

Best Price: $2.00

Buy New $9.95

(as of 09:55 UTC - Details)

The Great Deformation:...

Best Price: $2.00

Buy New $9.95

(as of 09:55 UTC - Details)

Investing in large-scale cannabis cultivation today is like playing the end of alcohol prohibition by buying a hops farm. What investors should be focused on is controlling brands and distribution points for those brands.

Simply put, in the longer term it will be simply untenable for large-scale indoor cannabis producers in the United States and Canada to survive. Even greenhouse producers in most regions of the country will struggle to compete with low-cost production on the west coast and Latin America. For those companies currently spending millions of dollars building out state-of-the-art, high-tech, clean-room cultivation facilities across Pennsylvania, New York, Florida, Massachusetts, and elsewhere in the United States be warned, you may find yourselves stick with a beautiful state-of-the-art dinosaur.

Indeed, today’s $1,700 per pound price for cannabis flower in the relatively free republic of Colorado is still at pre-1933 moonshine scale. By contrast, the wholesale price per pound of corn, soybeans, lentils and lettuce is $0.10, $0.15, $1.50 and $2.50, respectively.

We’d guess that cannabis is more in the lentil and lettuce aisle than the corn or soy oil shelves, but even then if it is 40X more valuable than lettuce on the free market for large scale cultivation, it is still priced 17X too high.

So $25,000 of market cap per pound of output for stuff that not too far down the road might sell for $100 per pound and generate $10 per pound of profits?

We’ll take the unders. But we must also note that Tilray is not an aberration – today’s reefer madness is only a metaphor for the insanity all around.

And on that score, Zero Hedge said it well this AM with respect to the much larger and more consequential raging mania in the junk debt markets:

It’s party time for zombie companies everywhere as “high yield” is now officially “low yield.”

The record stock market euphoria and the resulting “dash for trash” seen in recent days as pennystock after pennystock has exploded higher on the back of bull raids orchestrated by redditors and complicit hedge fund managers, has spilled over into the junk bond market where the average yield on US junk bonds just dropped below 4% for the first time ever as investors keep piling into an asset class historically known for its “high yields” (hence the name), although if sub-4% is considered high then there is a problem.

As indicated in the chart below, the Bloomberg Barclays U.S. Corporate High-Yield index dipped to 3.96% on Monday, its sixth straight session of declines, and now stands at the lowest level in history.

But here’s the thing. In the best of worlds junk bonds tend to produce 3-5% losses over the business cycle, and the trend inflation rate is still running at about 2%. That is to say, relative to a 5% to 7% margin for losses and inflation, junk bond yields are absurdly under-priced and reflect nothing more than the speculative frenzy of the liquidity-driven hordes.

As a measure of how unhinged the high yield markets have become, note the green arrow in the chart below. Today’s junk bond yield is lower than the risk-free 10-year UST was a recently as 2010!

Not surprisingly, fund managers have dashed for trash notwithstanding the horrible economics because the alternative of a 1.1% yield on 10-year treasuries is even more ridiculous.

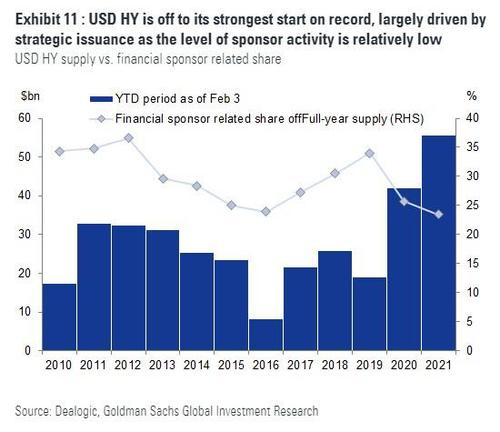

Accordingly, new junk bond issues through February 3rd topped $55 billion, a figure which towers above the comparable period all prior years including the pre-Covid boom last year.

Needless to say, this massive cash raise is not going into productive investment in plant, equipment, technology or human resources. It’s just financial engineering whereby the cash flows and balance sheets of operating companies are leveraged to the hilt in order to disgorge stock buybacks, recaps and buyouts into the speculative maws of Wall Street.

As a result of this relentless demand for junk, a majority of new issues, even those rated in the riskiest CCC tier, have been hugely oversubscribed.

In fact, according to Credit Suisse, this year has witnessed a red hot rally in lower quality HY paper bearing the “triple hooks”. That is to say, the kind of junk paper that has historically been a way station to chapter 11 and which has produced losses in excess of 20% is now trading at record lows at 6.7%.

Needless to say, this avalanche of junk is great news for zombie corporations which will be able to obtain cheap access to cash, allowing them to continue their cash burning, deflationary existence for another year or two or even longer.

Peak Trump: The Undrai...

Best Price: $12.72

Buy New $43.07

(as of 11:40 UTC - Details)

Peak Trump: The Undrai...

Best Price: $12.72

Buy New $43.07

(as of 11:40 UTC - Details)

Moreover, when the “market” dashes for trash at off-the-charts 9X EBITDA multiples, it only encourages more leveraged financial engineering and more companies to load up their balance sheets with ultra-cheap debt.

Of course, when the systematic effect of Fed money-pumping is to keep zombie corporations on life-support indefinitely, then it can be well and truly said that the Eccles Building has become a veritable national menace. That’s because debt-ridden zombie companies are the very inverse of Schumpeter’s “creative destruction”.

Rather than permitting the free market to cleanse the economy of inefficient, outmoded and uncompetitive business operations, the Fed’s drastic interest rate repression and deep subsidization of speculation locks them in, thereby impairing the growth-fueling reallocation and repurposing of labor and capital resources on which capitalist prosperity depends.

So, yes, it’s not just the homegamers in mom’s basement who are smoking something. The folks in the Eccles Building who are enabling this madness are giving the notion of hallucination an altogether new definition.

PEAK TRUMP, IMPENDING CRISES, ESSENTIAL INFO & ACTION

Reprinted with permission from David Stockman’s Contra Corner.

Top Dr. Mercola Videos Banned by Google

Top Dr. Mercola Videos Banned by Google