Subprime Auto Delinquency Rates at Levels Higher than During the Financial Crisis

May 19, 2018

Here’s another sign that the air is starting to come out of the subprime automobile bubble.

The default rate on subprime auto loans has reached levels higher than we saw during the financial crisis. As a result, lenders are shutting off the easy money spigot. That’s bad news for the auto industry.

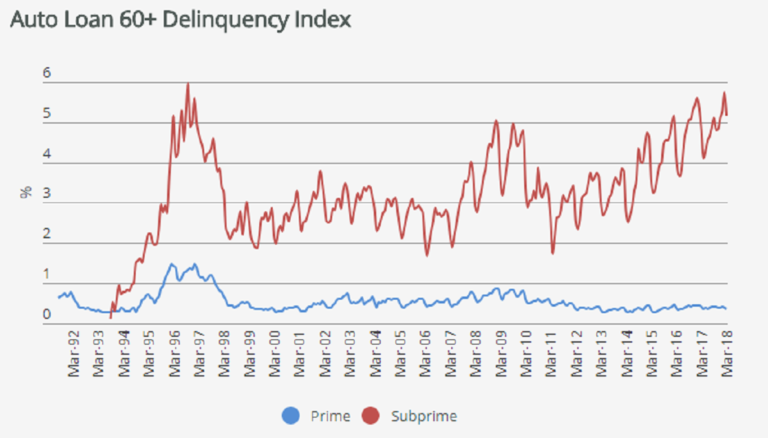

According to the latest data from Fitch and reported by Bloomberg, the delinquency rate for auto loans more than 60 days past due hit 5.8% in March. That’s the highest level since 1996. The default rate during the peak of the financial crisis came in at around 5%.

And this is happening while the economy is supposedly doing great. What will delinquency rates look like when the economy goes bad?

So far, small companies have borne the brunt of rising defaults. According to Bloomberg, “an influx of generally riskier, smaller lenders flooded into it in the post-crisis years, bankrolled by private-equity money, which pursued the riskiest borrowers in order to stay competitive.” Those companies are beginning to go belly-up. But as ZeroHedge noted, “we all know what comes next: the larger companies go bust, inciting real capitulation.”

Meanwhile, the number of auto loans and leases extended to customers with shaky credit has plunged, falling almost 10% from a year earlier in January, according to Equifax. Auto-lease origination to high-risk borrowers decreased by 13.5%.

How an Economy Grows a...

Best Price: $1.99

Buy New $7.20

(as of 11:05 UTC - Details)

How an Economy Grows a...

Best Price: $1.99

Buy New $7.20

(as of 11:05 UTC - Details)

The auto industry faces a double-whammy. With defaults on the rise and tighter lending standards, its pool of customers is shrinking. Meanwhile, rising interest rates will push the price of vehicles even higher than they already are – and they are high. That means even more consumers squeezed out of the market.

As we reported last month, the price of a new car has risen to the point that the vast majority of Americans simply can’t plunk down some cash and drive off the lot. Even a decent used car is out of reach for most American consumers. The average price for a new vehicle is at a record high $31,099, and the average used car price is also in record territory – $19,589.

This means borrowing and lots of it. Americans have to borrow more for longer periods of time in order to bring home that new car. The average auto loan has hit a record length of 69 months. The average monthly payment now stands at a whopping $515 per month.

As Bloomberg noted, the pain among small auto lenders “parallels with the subprime mortgage crisis last decade, when the demise of finance companies like Ownit Mortgage and Sebring Capital Partners were a harbinger that bigger losses for the financial system were coming.”

The Real Crash: Americ...

Best Price: $3.00

Buy New $9.55

(as of 12:25 UTC - Details)

The Real Crash: Americ...

Best Price: $3.00

Buy New $9.55

(as of 12:25 UTC - Details)

The common denominator here: rising interest rates. Easy money pumped up both the housing and auto loan bubble. When the Fed takes away the punchbowl, bubbles burst.

As Ryan McMaken explained in an article at the Mises Wire, the auto industry has survived on cheap money.

Ultra-cheap borrowing costs have allowed auto dealers to push ever larger auto purchases by just telling new buyers to ‘finance it.’ This had been going on well before the current era of post-financial-crisis ‘stimulus,’ but the Fed’s quantitative easing after 2008 helped prolong the era of cheap auto debt far longer than many might have expected. If it weren’t for this, we’d likely see auto sales totals that are far worse than what we’ve been seeing.”

If the Federal Reserve keeps pushing up interest rates up, it could spell big trouble for the auto industry – a key part of the US economy. This is another example of what happens in an economy dependent on Federal Reserve monetary policy to keep it running. It’s party-hardy as long as the punch bowl is full. But when it starts to empty out, the party-goers throw a fit.

Reprinted with permission from SchiffGold.com.

Copyright © 2018 SchiffGold.com

Are Boycotts Ethical?

Are Boycotts Ethical?