Subprime Mortgages Among Fastest Growing Investments for US Banks

April 7, 2018

“As a dog returns to its vomit, so fools repeat their folly.” – Prov. 26:11

It appears there is some repeat folly brewing.

Remember subprime mortgages? Well, they’re back.

According to an article published by SovereignMan, subprime volume at US banks doubled over the last 12 months and it is on pace to double again this year. Subprime loans rank among the fastest growing investments for banks in the US.

SovereignMan has dubbed these foolish bankers “financius dumbassus” to emphasize the folly of repeating a practice that nearly brought down the entire global economy.

Bottom line– financius dumbassus is once again back to its old ways… making risky loans to borrowers with pitiful credit. What could possibly go wrong? Leave it to financius dumbassus to try the same thing again and expect a different result. It’s textbook insanity.”

How an Economy Grows a...

Best Price: $1.99

Buy New $7.20

(as of 11:05 UTC - Details)

How an Economy Grows a...

Best Price: $1.99

Buy New $7.20

(as of 11:05 UTC - Details)

But this isn’t an identical repeat performance. The banking industry has changed the name. We no longer call these risky loans “subprime.” Now we call them “non-QM,” meaning “non-qualified mortgage.” But we are talking about essentially the same thing. Banks extend loans to borrowers who don’t qualify for conventional mortgages because they have bad credit ratings or don’t have enough money to make a down payment.

Indeed, we’ve seen this folly before, and as SovereignMan points out, nearly the entire financial system got into the game the last time around.

The mortgage brokers raked in huge fees for closing individual loans. The investment bankers made money packaging the loans into subprime bonds. And the ratings agencies (like S&P and Moody’s) made money slapping pristine ‘AAA’ ratings on these bonds, essentially promising the world that they were RISK FREE. Looking back they obviously weren’t risk free. Banks were making risky loans to borrowers who had a history of not paying their debts based on the premise that home prices only increase in value. And when home prices started to fall, the entire apparatus collapsed in late 2008.

The Real Crash: Americ...

Best Price: $3.00

Buy New $9.55

(as of 12:25 UTC - Details)

The Real Crash: Americ...

Best Price: $3.00

Buy New $9.55

(as of 12:25 UTC - Details)

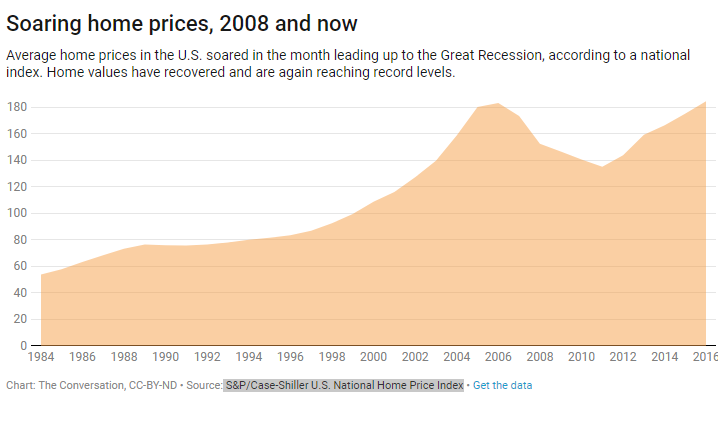

And guess what? We also have another housing bubble blowing up.

We don’t have the same kind of housing bubble today that we did in 2007. It’s more like housing bubble 2.0. Nevertheless, we still have the same fundamental problem. People with average incomes cannot afford to buy an average-priced home.

In other words, the rising price of homes has priced a lot of everyday Americans out of the market. So to keep the ball rolling, banks are stepping up to the plate and loaning them money anyway – banking (pun intended) on the fact that the value of the house will cover their risk.

This isn’t to say we are poised for a repeat of 2007-2008. There are even bigger bubbles that could burst first. But this is yet another sign that everything isn’t as great as the mainstream would have you believe.

And it also demonstrates an ugly truth. People don’t learn. Or they forget. Especially when there is a dollar to be made today.

Einstein supposedly said, “insanity is doing the same thing over and over again expecting a different result.” Central bankers at the Fed sure do seem to suffer from this affliction – along with a lot of others in the banking system.

Like a dog…

Reprinted with permission from SchiffGold.com.

Copyright © 2018 SchiffGold.com

Anarchy and Voluntaryism

Anarchy and Voluntaryism