A few years ago on these pages, I harshly criticized an article urging New Yorkers to “eat local,” and went so far as to dub the young lady’s column, “The worst economics article ever.” I am here to report that her record has been smashed. Floyd Norris’s recent New York Times article on the greenback is hands down the worst economics article I have ever read. Not only is it jam-packed full of false history, but it uses the falsehoods to justify monstrous crimes, both in the past and present.

The reader with a strong stomach will have to click the above link to appreciate the full enormity of Norris’s accomplishment, but for those with limited attention spans I’ll detail some of its biggest problems below.

Bernanke Saved the Credit Markets?

The article opens up with claims about the health of the world economy that are misleading at best:

Six months after the financial world seemed to be coming to an end, the world’s economies appear to be recovering. Banks that seemed to be on the brink of failure less than a year ago are now able to pay back investments made by the Treasury.

It is too early to declare victory, but the world looks much safer than it did only a few months ago. Credit markets are recovering, to the point that the junk bond market will have its best year ever if it manages not to lose any money over the rest of 2009. The stock market has just finished its best six months since 1938.

If victory is to be had, it will owe a lot to the willingness of American policy makers to set aside cherished policies and simply create money. And that is one reason it is appropriate to pause and celebrate an unheralded bicentennial: The father of the greenback, Elbridge Gerry Spaulding, who was born 200 years ago, in 1809. (emphasis added)

Now hold on just a second. I want to challenge this claim that things are now recovering. Concerning banks paying back their TARP money, I have dealt with that issue here. Regarding the stock market, Norris is right: it’s way up (so far) in 2009. But I don’t remember Henry Paulson, Timothy Geithner, Ben Bernanke, or Presidents Bush and Obama ever justifying their rescue programs by saying, “We need to do this to resuscitate the stock market.” I grant you, they may (and probably did) say that the stock market would be helped by their programs, but pumping up stock prices was never the justification given to the American public.

As I recall, the justifications were all about J-O-B-S. Specifically, Paulson told Congress that he needed the $700 billion TARP package to save the banks, not because anybody cares about Wall Street fat cats, but because plenty of businesses needed short-term financing to meet their payrolls. (A lot of us wondered at the time what types of businesses paid their employees with borrowed money, but solving that kind of mystery is why the Treasury secretary makes the big bucks.) And of course, the Obama administration warned everyone that without pushing through the $787 billion “stimulus” package, aggregate demand would collapse even more and the unemployment rate would skyrocket.

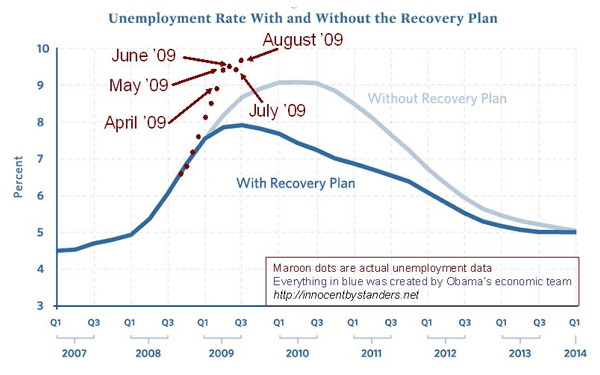

So let’s check up on these two things. Below is a chart (reproduced from Greg Mankiw’s blog) showing what the administration forecasts were for the unemployment rate, with and without the stimulus package:

(Original image source here.)

(Original image source here.)

The Politically Incorr...

Best Price: $5.62

Buy New $15.94

(as of 05:25 UTC - Details)

The Politically Incorr...

Best Price: $5.62

Buy New $15.94

(as of 05:25 UTC - Details)

So just to be clear, Obama’s economic team warned America that without their stimulus plan, unemployment might flirt with 9 percent, whereas with the Keynesian shot in the arm, unemployment wouldn’t break 8 percent. After getting the stimulus, the actual unemployment rate is now nearly 10 percent.

It’s true, this awkward set of facts doesn’t prove that the stimulus was a bad idea. It is theoretically possible that Obama really did inherit an economy in worse shape than his team realized back in January, and that without the stimulus, the actual unemployment rate now would be, say, 14 percent. But since plenty of free-market economists were warning that deficit spending just transfers productive resources into the bloated government sector, doing nothing to really help the economy, the above chart should be embarrassing indeed for the Keynesians. Yes, it’s not the whole story, but it certainly is evidence that the free marketeers were right.

Now what about this issue of the credit markets? Norris isn’t original in his description; the conventional wisdom now is that the credit markets were on the verge of collapse, but that the unprecedented Treasury and Fed countermeasures (concentrated in September and October 2008) turned the situation around. According to this story, it wasn’t just the overleveraged Wall Street firms that were in trouble; the amount of credit available to regular, mid-sized businesses — who hadn’t dabbled in mortgage-backed securities or credit default swaps — was shriveling up. Paulson and Bernanke swooped in to save the day.

Suppose for a moment, just for fun, that this story about the credit markets is just as backwards as the story about the stimulus package. What would that mean, if the story is 100% wrong? Well, I guess it would mean that the total amount of business loans was actually rising and in fact at an all-time high, up to the point when Paulson and Bernanke decided to throw caution to the winds. And then after their heroic intervention, the total amount of business loans fell like a stone. Can we agree that something like this would mean the story Norris has repeated is exactly backwards? Well feast your eyes on this:

Now let’s be fair. Someone could plausibly argue that the business loans dried up when they did, in response to the collapse of Lehman and so forth. In this view, the drop that we see in the chart above would have been far greater were it not for the Fed’s rescue efforts and TARP. (There are other indicators people point to, such as the spreads between different types of debt.) But notice the similarity with the unemployment situation. Here too, the raw facts and Occam’s razor suggest that the interventions have hurt the ability of average businesses (not just the huge beneficiaries of the bailouts) to obtain financing. The chart above doesn’t prove that the TARP and Fed rescues were bad, but by no means should Norris be talking as if the recovery of the credit markets is a self-evident fact.