The Mechanics Behind a Credit Crisis

January 19, 2024

Imbalances in the global fiat credit system are enormous, with foreign ownership of dollars overhanging both foreign exchanges and securities markets. Meanwhile, Keynesian and monetarist hopes that lower interest rates can be implemented to keep things just bubbling along is blinding investors to the real risks.

It is wrongly believed by nearly everyone that lower interest rates are on the way and will stay down. Other than perhaps a minor decline being a self-fulfilling prophecy, in practice the reluctance of banks to lend to businesses will keep rates high. And the redirection of bank credit from productive use to the US Government financing its huge budget deficits by issuing treasury bills is highly inflationary.

This is bound to lead to significantly higher interest rates in time. And higher interest rates will threaten to collapse the entire credit system.

Irving Fisher’s collateral doom-loop, whereby falling collateral values lead to further collateral liquidation could also come into play. Thinly capitalised regulated exchanges will be a weak point, requiring the entire DTC ledger to be corralled into keeping them functioning. Nothing will be safe.

Jade Leaf Matcha Organ...

Check Amazon for Pricing.

Jade Leaf Matcha Organ...

Check Amazon for Pricing.

And those who think that they can protect themselves by buying gold ETFs will probably find that the underlying bullion is diverted “in the interests of the state”, leaving them with vacuous paper promises as their only comfort.

No wonder everyone thinks interest rates must come down. If they don’t, the outcome is too horrible to contemplate.

In today’s complex markets, it is difficult for the layman to understand their workings. It has always been about central and commercial bank credit, which must never be confused with money, and which from the dawn of history has been physical metal. Today, we can say it is almost exclusively gold. But that is the medium of exchange of last resort, hoarded by individuals, and in recent decades increasingly by central banks and Asian interests.

The layman’s understanding of the difference between credit and money is further undermined by state propaganda which we can trace back to the suspension of the gold standard in America in 1933, which de facto had lasted since the 1850s, and de jure since 1900. This was followed by the naked attempt to expel gold from the monetary system entirely by ending the Bretton Woods Agreement in 1971. Subsequent events have intensified monetary disinformation, leading to a global fiat money system based on the US dollar but detached in value from gold entirely.

In order to give us all the illusion of price stability, the Breton Woods Agreement had been designed to promote the dollar as a gold substitute for all other currencies. Since its suspension, to maintain the dollar’s credibility the US Government increasingly resorted to market manipulation. First, they tried selling gold into the market in the early seventies, which was readily bought and failed to stop the gold price from continuing to rise. The next wheeze was to create artificial demand for dollars in an attempt to support its purchasing power, measured against commodities and other currencies. This led to the expansion of derivative markets, which diverted speculative demand for commodities thereby suppressing their prices below where they would otherwise be. The expansion of the London bullion market which created paper gold, and demand for the dollar not just to settle cross-border trade and commodity pricing but to replace gold in central banks’ reserves was all part of the deception.

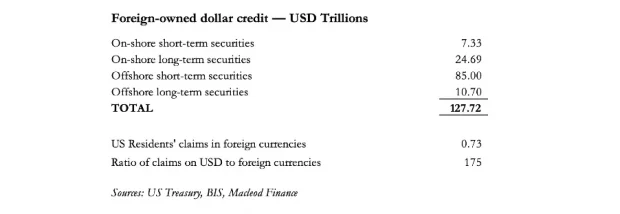

Over the fifty-two years since Bretton Woods was suspended, huge dollar imbalances have accumulated. A table of recent estimated bank and shadow bank dollar balances, onshore and offshore, is shown below.

The offshore element is considerably larger than that registered in the US Treasury’s TIC numbers for onshore securities, which in itself tells us that foreign interest in onshore dollar investments and bank balances only exceeds US GDP by a fair margin. The offshore element is based on the Bank for International Settlements analysis of dollar deposits and short-term obligations outside the US financial system which we can equate with the eurodollar market. In the main, they are currency forwards and swaps where one leg is in US dollars. By way of contrast, US Residents’ claims in foreign currencies are remarkably small. But this is because long-term securities are held overwhelmingly in ADR form: ADRs are denominated in dollars and sales of them by US investors do not give rise to foreign currency exposure.

Mr. Bird Woodpecker Fe...

Check Amazon for Pricing.

Mr. Bird Woodpecker Fe...

Check Amazon for Pricing.

Now that the financial bubble inflated by zero and negative interest rates is being lanced, these balances are bound to diminish. We can see why this is the case just with onshore long-term securities, comprised of bonds and equities, to which we must add the estimated $10.7 trillion of eurodollar long term bonds. That’s $35 trillion in foreign-owned long-term investments in bonds and equities overhanging US financial markets, whose values are at risk from higher bond yields. Including additional offshore short-term deposits and foreign exchange positions in dollars, the total of $127.7 trillion is 175 times the foreign currencies held by US residents, available to absorb foreign dollar liquidation. This imbalance between foreign ownership of dollars and the availability of foreign currencies in US hands to absorb foreign dollar liquidation is simply staggering in its potential impact on the dollar.

The importance of this lop-sidedness cannot be over emphasised. A banking crisis, bear market in securities, geopolitical developments, or more likely some sort of combination of the three could lead to a rapid collapse of the entire American credit system. And the future of the massive dollar credit structure initially depends on interest rates and bond yields declining convincingly from current levels, and inflation remaining subdued.

This is the stuff of dreams, not reality.

Copyright © Alasdair Macleod

World Economic Forum: Government Is Obsolete

World Economic Forum: Government Is Obsolete