"Janet Yellen Powell Puts" On Some Pants And A Tie

November 6, 2017

It can’t get any worse than this. Jerome Powell is a Wall Street-coddling Keynesian and Washington lifer who passes for a Janet Yellen replica – that is, save for his tie and trousers and his as yet underdeveloped capacity to whine pedantically.

During his years on the Fed since May 2012, Powell has voted approximately 44 times to drastically falsify interest rates and to recklessly and fraudulently monetize trillions of the public debt. That is, Powell has been all-in for a destructive central banking regime that is literally asphyxiating capitalist prosperity in America.

We will get to the latter in more detail momentarily, but just consider the plight of bank account savers during the 65 months “Jay” has served on the Federal Reserve Board. They have been continuously savaged by negative real interest rates averaging -1.8% per year. That cumulates to a 9% confiscation of inflation-adjusted principal during that five and one-half year period, but this purported Republican dissented not a single time.

And now he is being appointed Fed Chairman by a purported Republican President!

At this point, therefore, it can be well and truly said that Wall Street owns the nation’s central bank and that the Republican party has morphed into a gang of dutiful handmaidens. Any semblance of fidelity to sound money and free market capitalism – of the type, for instance, so brilliantly articulated by Treasury Secretary Bill Simon during Ford’s time and George Humphreys during the Eisenhower era – has been lost in the fog of history.

Not only did Republican presidents appoint the scourges of Greenspan and Bernanke, but the GOP standard bearers thereafter have essentially embraced more of the same monetary central planning. During the 2008 campaign, for example, Senator McCain’s chief economic advisory was Mark Zandi of Moody’s – a Fed sycophant and Keynesian “stimulus” devotee if there ever was one. And Mitt Romney’s top economic advisor in 2012 was professor R. Glenn Hubbard of Columbia, who averred at the time that Bernanke was doing a swell job.

Trumped! A Nation on t...

Best Price: $2.05

Buy New $9.50

(as of 06:30 UTC - Details)

Trumped! A Nation on t...

Best Price: $2.05

Buy New $9.50

(as of 06:30 UTC - Details)

Yes, we know that the Donald came to the Oval Office with a giant disability on the matter of sound money.

To wit, he claims to be a billionaire and perhaps is. But if so, it wasn’t owing to the genius and business acumen domiciled in Trump Tower; it was solely and completely due to the fact that the Donald’s 40-year career as a leveraged real estate developer was flattered beyond measure by the cheap debt and serial bubbles that have been the essence of central bank policy since Volcker was fired in 1987.

So we did take his campaign attack on the Fed’s “big, fat, ugly bubble” with several grains of salt, and knew that his self-characterization as a “low interest man” did not bode well for his approach to filling the raft of vacancies at the Fed.

Still, the choice of Powell is a shocker. This guy is so deep in the tank for the speculative classes and such a mechanical Keynesian that there is really no hope at all that the era of Bubble Finance will end – that is, voluntarily and without a thundering financial crash.

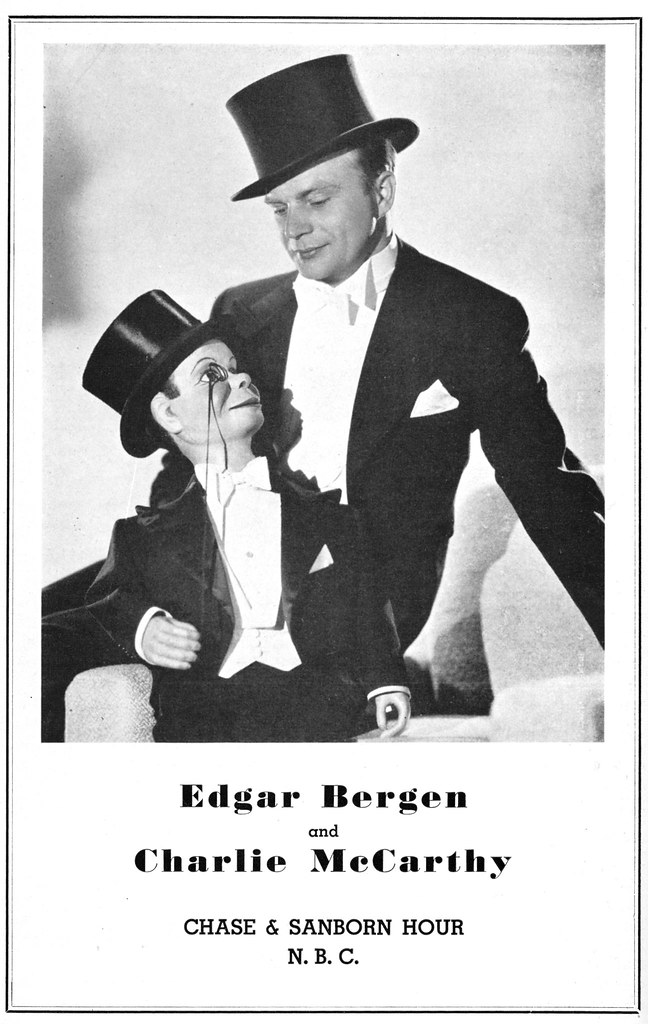

Indeed, Powell is so mired in Fed group think with respect to the ridiculous fixation on 2.00% inflation and the utterly discredited Phillips Curve and DSGE (dynamic stochastic general equilibrium) models that you might well think he was Charlie McCarthy to Janet Yellen’s Edgar Bergen.

Thus, in almost identical words to Yellen’s blathering at her last presser, Powell has been mystified by an alleged inflation shortfall and gums at will about too much slack in his bathtub model of the US economy:

“Inflation is a little bit below target, and it’s kind of a mystery,” he told CNBC in August. “You would have expected, given that we’re getting tighter labor markets, that we’d have a little higher inflation. I think that what that gives us is the ability to be patient.”

The relationship between slack and inflation has weakened substantially over the years,” Powell said in June 2016. “In addition, inflation depends importantly on the inflation expectations of workers and firms. A widely shared view among economists today is that, unlike during the 1970s, expectations are no longer heavily influenced by fluctuations in inflation, but are fairly constant, or anchored. For both these reasons, inflation has become less responsive to cyclical changes in the economy.”

“While inflation expectations seem to me to remain reasonably well anchored, it is essential that they remain so,” he said. “The only way to assure that anchoring is to achieve actual inflation of 2 percent, and I am strongly committed to that objective.”

Folks, that’s just the group think voodoo economics that has metastasized in the Eccles Building for the last several decades. Indeed, the latter now sits at ground zero in the Swamp, and the Donald didn’t even bother to look beyond its walls to fill a job that in many ways is more crucial and powerful than his own.

As the Donald would tweet it, SHAME!

Nevertheless, there can be no doubt that Powell was the #1, #2, and 3# pick of the Vampire Squid after its own nominee, Gary Cohn, stepped in some deep dodoo during the Charlottesville contretemps. The tip-off is Powell’s above reiteration of the 2% inflation goal.

The latter has absolutely nothing to do with genuine economic growth and main street prosperity. It is merely a ritual incantation used to justify the Fed’s plenary intrusion in the financial markets and relentless manipulation of the most important prices in all of capitalism: That is, the price of money, debt, the shape of the yield curve and the valuation of equities and other risk assets.

As we said on Fox Business last night (video below), after 100 months of so-called business expansion – the third longest on record – the idea that the money market rate should still be 1.13% is preposterous because in real terms in still negative. It is a massive open invitation to Wall Street speculators to buy any financial asset with a yield or prospect of short-term appreciation and fund them with free overnight carry administered, enforced and guaranteed by the central bank.

Indeed, Powell is so clueless on this matter that he actually describes the Fed’s fundamental policy tool as an exercise in administering prices in the money and debt markets, thereby implying that the 12 members of the FOMC know better than the millions of traders, investors and arbitrageurs who inhabit the casino, and that through the frail instrument of interest rate pegging can command the performance of a $19 trillion economy.

Moreover, rather than arguing for pegging as a one-time, extraordinary response to a putative 500-year flood type of financial crisis, Powell argues that it constitutes a permanent regime of control. That is, capitalism is allegedly so fragile, unstable and disaster prone that it requires permanent guard rails and balancing wheels supplied by the FOMC in it purported infinite wisdom:

Powell seems to be in agreement stating in June of this year that “To affect financial conditions, the Federal Reserve has therefore used administered rates, including the interest rate paid on excess reserves (IOER) and, more recently, the offering rate of the overnight reverse repurchase agreement (ON RRP) facility. This approach, sometimes referred to as a “floor system,” is simple to operate and has provided good control over the federal funds rate. In November 2016, when the Committee discussed using a floor system as part of its longer-run framework, I was among those who saw such an approach as “likely to be relatively simple and efficient to administer, relatively straightforward to communicate, and effective in enabling interest rate control across a wide range of circumstances.”

The Great Deformation:...

Best Price: $4.26

Buy New $8.99

(as of 05:50 UTC - Details)

The above hogwash is stunning proof that Greenspan-Bernanke-Yellen-Powell style monetary central planning is a clear and present danger to capitalist prosperity. It amounts to a clueless confession of willful incompetence, and evidence that Powell and the rest of the FOMC – are so mesmerized by Keynesian academic models that they can’t see the real world starring them in the face.

The Great Deformation:...

Best Price: $4.26

Buy New $8.99

(as of 05:50 UTC - Details)

The above hogwash is stunning proof that Greenspan-Bernanke-Yellen-Powell style monetary central planning is a clear and present danger to capitalist prosperity. It amounts to a clueless confession of willful incompetence, and evidence that Powell and the rest of the FOMC – are so mesmerized by Keynesian academic models that they can’t see the real world starring them in the face.

What’s right in front of their collective noses, of course, is a domestic and global financial system that is everywhere booby-trapped with massive and incendiary financial bubbles, unsustainable leverage in both overt and covert forms (i.e. options), and relentless, liquidity-fueled speculation that infects the very warp and woof of most financial markets.

Even the core blue-chip 10-year UST market is a speculators’ haven where on the margin pricing is driven by complex, leveraged arbitrages, not the bid of trust department managers in behalf of widows and orphans.

Indeed, the evidence of an impending financial blow-up is palpable and plenary.

There is no other way to describe European junk bond yields at 2% and therefore below the U.S. Treasury; or the Russell 2000 trading at 95X earnings in an economic backdrop where most activity measures – from auto sales ex-hurricane replacement, to housing, restaurant sales, manufacturing production, business investment, exports, construction spending – are clearly rolling over.

Likewise, there is the insanity in the momo precincts of the stock market where the likes of Amazon and Netflix trade at 280X and 200X net income, respectively; or where the giant fake auto company, Tesla, trades at an infinite PE multiple after 10 years of cumulative losses totaling $4.5 billion and which, at a market cap of $50 billion, is valued the same as Ford and nearly equal to GM. Between them, the latter sold 10 million cars last year – 125 times more than Tesla – and booked $7.5 billion of profits or well more than the latter’s total loss-making sales.

You only need read the latest Fed minutes – which Powell fully subscribed to – in order to realize that the Fed’s scribe hit the “delete” key when the discussion turned to financial bubbles. Then again, perhaps the myopic lenses of their Keynesian beer goggles filtered out entirely the above evidence of today’s raging mania in risk asset markets, thereby ensuring that our monetary central planners will be taken by “surprise” for the third time this century.

The screaming disconnect implicit in Fed policy is evident when you compare Powell’s group-think complacency with the FOMC’s fastidious preoccupation with its preferred short-term inflation measures. That is, both the CPI and the PCE deflator have been in the 1.4% to 2.2% corridor for several months now, but the FOMC remains preoccupied with “low readings”.

Yet there is not a shred of evidence that 50 basis points of difference in a generic market basket of prices (which no one actually buys) makes any difference whatsoever to economic function in the main street economy. Well, except for pensioners, savers and most workers, whose purchasing power will fall further behind the closer the Fed gets to its magic 2.00% inflation reading.

We choose to express the Fed’s inflation goal to the second decimal point to highlight the lunacy of the entire inflation targeting regime. In fact, there is a breathtaking mismatch between the Fed’s inability to see a $200-300 billion bubble of bottled air at Amazon, which enables it to ignore profits and investment returns in order to pursue a scorched earth policy of predation and destruction across the American retail landscape, and the fact that Fed heads like Powell spend countless hours down on their hands and knees with magnifying glass parsing utterly trivial differences in the PCE deflator readings.

Some members stressed the importance of underscoring the Committee’s commitment to its (2%) inflation objective. These members emphasized that, in considering the timing of further adjustments in the federal funds rate, they would be evaluating incoming information to assess the likelihood that recent low readings on inflation were transitory and that inflation was again on a trajectory consistent with achieving the Committee’s 2 percent objective over the medium term.

In short, this is a case of missing the forest for the trees like no other, and exposes the screaming contradiction at the heart of our rotten regime of monetary central planning.

Today’s Keynesian central bankers – and Powell is surely one straight from central casting – are always aiming to enhance, uplift and stimulate the main street economy but to do so they must detour through the canyons of Wall Street because that’s where their instruments of control reside.

As we indicated above, the Fed seeks to transmit its stimulus policies through the money markets by pegging overnight funding rates including Fed funds and through the fixed income and other securities markets, where its open markets desk drives the level and shape of the fixed income yield curve through bond purchases with fiat credits.

In this context, it is important to note that Janet Yellen, Jerome Powell and their ilk are playing a totally different game than their Keynesian grandfathers such as professors James Tobin, Walter Heller and Paul Samuelson. The latter were primarily fiscalists, which meant that if they wanted more housing production, for example, they would turn to builder subsidies or tax credits.

Likewise, if they felt the main street economy would have more zip with higher consumer spending, they would peddle tax rebates or increased entitlement benefits. And the same approach prevailed if more business investment was deemed to be helpful – as in Walter Heller’s (Kennedy’s chief economist) invention of the investment tax credit in 1962.

In a word, these grandfatherly Keynesians could do considerable long-run damage to capitalist prosperity and growth by causing resources to be channeled to sectors of the economy and purposes that deviated from market outcomes, and would thereby inevitably result in inefficiency, malinvestments and waste.

But the saving grace was transparency, targetability and limited collateral effects. Back in the 1970s, for example, the homebuilders and S&L industry were always looking to help the national economic good by offering first time buyer credits for new homes or rent subsidies to induce apartment construction. But you could measure the budget expense, debate the social cost/benefit equation and be reasonably sure that the subventions involved did not go into speculative schemes on Wall Street.

Yet here is exactly where Alan Greenspan and his successors and assigns – of whom Powell is the latest – committed the economic sin of the century. Greenspan was actually an anti-Keynesian in the old fashioned fiscalist sense and was a frequent comrade-in-arms with your editor in the budget battles of the early 1980s. Indeed, he helped us defeat every single Keynesian fiscal stimulus scheme that was floated on the Washington Swamp waters during the 1982-83 recession.

But apparently no good deed goes unpunished – especially when like Alan Greenspan you are always being too clever by half. That is, when he got to the Fed and soon had his hands all over the control dials on its printing presses, he had the epiphany that fiscal Keynesianism could be defeated permanently by seconding the job to the Fed.

Thus, if you wanted more housing starts, twist the interest rate dial to cheaper mortgages; or if you want more business investment, ginger the corporate stock and bond markets; or if you want more consumer spending, drive mortgage rates lower and housing prices higher so that households could supplement their earned incomes with MEW (mortgage equity withdrawal).

But as we said, this was way too clever by half. That’s because Greenspan’s backdoor Keynesianism unleashed the PhDs, bankers and policy apparatchiks that get appointed to the Fed to descend into the canyons of Wall Street en masse and continuously. So doing, it gave them license to fiddle and falsify all the financial asset prices that percolated through what had otherwise been the price discovery process of the free market.

From our vantage point 30-years later it is evident that this was a colossal mistake – the equivalent of inviting the Huns into Rome. And now, Jerome Powell is apparently the latest monetary Attila.

The fact is, the financial markets are the very heart of capitalism and constitute the delicate mainspring from which all else flows. Money, debt and other forms of capital most be priced efficiently, accurately and by the unfettered operation of the auction process for balancing supply and demand. That’s the only way you get allocative efficiency, financial discipline and rewards for true economic innovation, invention and entrepreneurial creativity all at the same time.

Accordingly, policy-making agents of the state should never, ever be allowed into the free market of finance. In fact, a policy regime that is explicitly posited on altering and falsifying financial asset prices is the mortal enemy of vibrant capitalism and true gains in living standards and wealth.

As we approach the third bubble crash of this century, the reason should be finally evident. Namely, financial repression massively incentivizes speculation, leveraged arbitrage, rent-seeking churning in the secondary markets and the diversion of real capital from the corporate sector and main street economy into financial engineering schemes which fuel even more speculation on Wall Street.

Thus, notwithstanding a tripling of business debt outstanding since the turn of the century, real net investment in productive business investment is 35% lower than it was in the year 2000.

Instead, the price falsification policies of the Fed have turned Wall Street into a gambling casino and the C-suites of Corporate America into financial engineering outfits. Accordingly, upwards of $15 trillion has been cycled back into Wall Street during the last decade in the form of stock buybacks, unearned dividends, M&A deals and LBOs and recaps that fueled stock market inflation, not real investment, growth and jobs.

There is a saying that if your only tool is a hammer everything looks like a nail. So with still another clueless Keynesian taking the helm at the Fed – and in complete denial about the monumental bubbles and financial stability risks all around – it can also be well and truly said that if your only policy tool is to falsify financial assets prices you will repeatedly end up inflating bubbles until they eventually crash – and never see them coming, to boot.

So if the state must give capitalism the “help” it doesn’t need – then at least bring back our Keynesian grandfathers to the fiscal arena. With $31 trillion of public debt already built in through 2027, they will get nowhere as the GOP tax-cutters are about to prove.

At least the fiscalists did not practice “trickle-up” economics by inflating bubbles that pleasure the 1%, but do nothing for the main street economy.

That’s the real irony. Modern central banking has not brought they ballyhooed Great Moderation, but a perverse cycle of periodic bubble collapses, which, in turn, induce corporate C-suites to attempt to protect their stock prices and options by throwing workers, assets and business infrastructure overboard in a desperate effort to appease the trading machines and gamblers on Wall Street.

So forget the Fed’s inflation targeting and its bathtub economics gibberish. Yellen, Powell and the rest of the Eccles Building posse are hopelessly Bubble Blind because inflating bubbles is the essence of what they do.

Then again, it is likely that Powell will be the last of the bubble blowers. Like Yellen he is so blind to the incendiary devices implanted throughout the financial system that he will likely continue her campaign to reload the Fed’s dry powder in order to combat the next recession somewhere down the road.

To that end, Powell has indicated he will pursue monetary policy normalization and balance sheet shrinkage until the Fed’s footings are rolled back to the $2.5 trillion neighborhood.

That means a year from now the Fed will be selling bonds at a $600 billion annual rate per its announced schedule and that will come atop a new borrowing requirement at the Treasury in the $1 trillion + annualized range. And since the law of supply and demand has not been repealed – that bond selling tsunami will surely cause a traumatic rise of bond yields across the entire spectrum.

In a word, “Janet Yellen Powell” has drawn the short straw. On his watch, the whole misbegotten enterprise of 30 years will blow sky high.

To that extent, the Great Disrupter once again today lived up to his historic mandate. But not in what the boys and girls and robo-machines on Wall Street would perceive as a “good way”.

To the contrary, they will learn the hard way about the end of Bubble Finance in the very near future.

Copyright © 2017 David Stockman

Diving Days

Diving Days