The S&P 500 moved by a mere 0.16% yesterday, making it 13 straight days in which the principal stock market average has changed by less than 0.3%. We mention that because it turns out that 13 straight days of virtual flat has never occurred before in records going back to 1927.

But despite the implication of the graph below, this is not about watching grass grow. That’s even given that the S&P’s closing prints over this unprecedented stretch of equipoise—–2474, 2473, 2473, 2470, 2477, 2478, 2475, 2472, 2470, 2476, 2478, 2472, 2477, 2481, respectively—–suggest exactly that.

To the contrary, it resembles something altogether different—– the absence of wave action in the eye of a hurricane, for example. Indeed, we have encased the graph in red to implicate the extreme dangers that are lurking all around.

These dangers start with the market’s demented internals—such as Amazon at 187X earnings, Netflix at 219X or Tesla valued at $62 billion. And the latter is after the company racked-up an unbroken string of cumulative losses which total $3.6 billion over the last decade, and with no profits visible anywhere on the horizon, either.

What is visible, by contrast, is the sheer mania in the capital markets which have fed its cash burning machine with more than $10 billion of capital—-including last night’s announcement that Tesla will issue $1.5 billion of junk bonds to fund the launch of its Model 3 “people’s car”.

Even by Elon Musk’s own admission, the launch of it’s first mass production car with a targeted build rate of 10,000 per week, compared to a maximum production rate of about 1,500 per week on its existing low-volume luxury models, will be an exercise in “manufacturing hell”. The potential for massive cost over-runs and expensive rework and parts scrappage on flawed vehicles coming off an untested assembly line, in fact, staggers the imagination of anyone who has been around the mass production auto business.

So does the fact that even prior to the Model 3 launch, Tesla burned through $3.2 billion of cash during the LTM period ending in June, and consumed $7.5 billion of cash since 2012. Yet the indicative pricing on the Musk’s new mess of junk is just 5.5%.

That’s right!

These are junk bonds with no upside issued by one of the most unhinged financial circus barkers of all time. Yet bond managers are so hungry for yield and have been so beaten down by years of Fed financial repression and drastic falsification of debt prices that they are accepting a yield on the Tesla junk that should actually be accorded a 10-year sovereign bond. Indeed, they are cued up in a line desperately waiting for an allocation of this toxic debris from underwriters.

Moreover, it’s not just the extreme high flyers that are at risk: The whole structure of financial asset prices has been wildly inflated by the central bank money printers, causing even the mundane to be radically mispriced.

For example, the 10-year average change in the CPI is 1.62% versus this morning’s 2.26% yield on the 10-year treasury note. That amounts to a real after-tax yield of 40 basis points—even if you credit the BLS’ inflation figures as measured by its sawed-off-ruler. Not only is this meager return far below historical levels, but it’s downright asinine given the Gong Show that has become a permanently modus operandi in the Imperial City.

Or consider the storied brand that trades under the symbol KO (Coca-Cola). It is currently valued at $195 billion, which represent 47X its LTM net income of $4.2 billion. But unlike Amazon, and more like the British armies at Dunkirk, Coca-Cola has been in retreat for years. It’s LTM sales of $39 billion are down nearly 20% from its 2012 peak and its LTM net income was down 40% from 2009. In fact, LTM net income of $4.2 billion was at the lowest level since March 2003!

Yes, there was a raft of charges and one-timers in KO’s financials, but with most of the big caps there always are. Yet even if you set aside the alleged distortions of GAAP accounting income, and look at free cash flow (which ignores non-cash charges in the current period such as for goodwill write-offs or employee severance to be paid out over time), the result is the same. With LTM free cash flow of about $6.5 billion, KO is currently trading at 30X, which makes no sense whatsoever for what in reality is a slowly dying brand and product.

Nevertheless, the penumbra of flashing red that surrounds the market’s eerie lull extends far beyond the egregious over-valuation of stocks and bonds. What really threatens is something that for want of a better term might be called: “regime change— homeland edition”.

In a word, the current blatant campaign by the Washington establishment to remove the Donald from office based on the completely phony—dare we say, trumped up—–Russia collusion story puts you in mind of John Adam’s famously pessimistic aphorism:

“Democracy never lasts long. It soon wastes, exhausts, and murders itself. There never was a democracy yet that did not commit suicide.”

It took awhile, but it can be said with some considerable certainty that if the Donald is given his last ride on the Nixon memorial helicopter, it will be the end of American democracy as we’ve known it. That’s because this time is very different than August 1974.

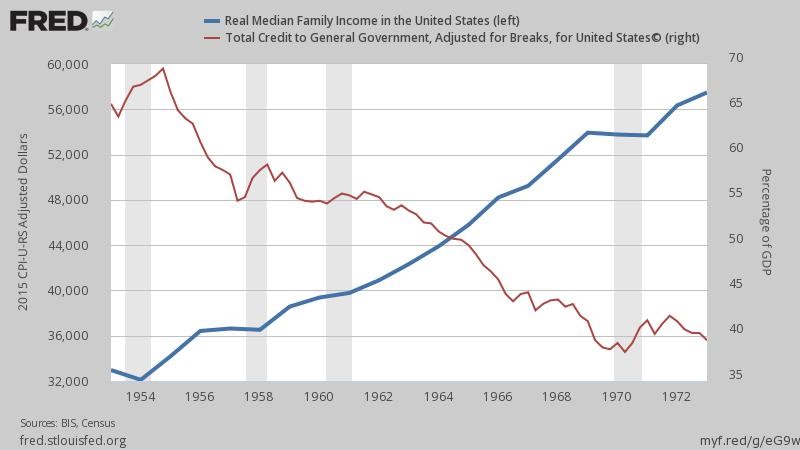

Back then, the US economy was still riding high from its post-war global dominance. During the previous 20 years real GDP had grown at a 3.8% compound rate and real median income had risen by 80% over the two-decade period. That’s about 3.1% per annum and means that the living standard was doubling every 20 years or so.

At the same time, Eisenhower had put budget policy back on a track of fiscal rectitude—-a position that his three successors had not really reversed, despite considerable effort. Accordingly, between 1953 and 1973 the nation’s general government debt share of GDP had declined sharply, falling from 67% to 40%.

As it happened, it took Ronald Reagan to reverse this beneficent trend and usher in the modern era of massive public borrowing eight years later. But at the time of Nixon’s removal, the nation’s fiscal accounts were in reasonable order, the entitlements explosion was still in its infancy and a high level of prosperity had generated reasonable contentment throughout the land.

As a young Congressional staffer, your editor was on the floor of the U.S. House when the baton was handed off to Gerry Ford and he delivered his magnificent speech assuring America that “our long nightmare is over”. It was a thrilling oration from a plain spoken mid-westerner, and it did pave the way for ameliorating the wounds engendered by the Watergate affair and for a reasonably orderly transition of government in a nation that did not yet really need Washington to prop up its economy and financial system.

The inverse pertains today in virtually every particular. When the 46th President of the United States, Mike Pence, takes to the well of the House to receive the baton, the nation’s real nightmare will be just beginning. Unlike 1974, the US economy and financial system will not take care of themselves because since the era of Reagan’s deficits and Greenspan’s Bubble Finance, they have become virtual wards of the state.

Indeed, Pence will not have a moment to bask in the relative economic quietude and spirit of national political unity that greeted Ford—- because there will be none of the latter and the former will be in instant crisis. The US is already fiscally ungovernable, but the run-up to and fact of Trump’s removal from office will cause it to burst wide open.

The only thing different about the chart below for 2000-2016 is that the “X” is reversed. The blue line of household income is still below its turn of the century level, meaning living standards have been shrinking, not doubling. What has doubled is the red line of government debt-to-GDP, which has soared from 55% to 106% of GDP.

What has also soared is the main street economy’s vulnerability to collapsing bubbles on Wall Street. When the Nixon stock bubble broke in 1973-74, the real economy took it in stride because the C-suites of corporate America were still in the business of producing widgets and building their base of productive assets. The 1974-1975 recession, in fact, was essentially an inventory liquidation and housing bust; it was triggered by Fed Chairman Arthur Burns when the explosion of bank credit growth, which the pusillanimous professor from Columbia University had fostered to insure Nixon’s 1972 re-election, had to be reined in.

By contrast, the C-suites today are in the business of financial engineering. That is, strip-mining their balance sheets and cash flows in order to fund stock buybacks, M&A deals and other leveraged maneuvers designed to goose their stock prices and fatten their stock option accounts.

Consequently, as the demise of the Orange Swan becomes ever more palpable and the Imperial City becomes embroiled in a thundering donnybrook over the debt ceiling and continuing resolutions—-that is, when the machinery of fiscal governance becomes hopelessly paralyzed—-the egregiously inflated stock and bond indices will come tumbling down owing to the shock and confusion it will generate in the casino.

And in that event, the C-suites of corporate America will drive the final nail in the coffin of the present fantasy world. That is, top corporate executives and boards will do what they did in the fall and winter of 2008-2009. In the wake of crashing stock prices they will energetically and wantonly throw labor, facilities and balance sheet assets overboard in a desperate effort to appease the Wall Street speculators and hedge funds, thereby hoping (vainly) to keep their stock options above water.

So doing, they will catalyze the kind of instant recession that struck violently and unexpectedly in Q4 of 2008.

Needless to say, there will be hell to pay in Flyover America when voters in the red counties and precincts are hit with the double whammy of losing their political champion and their jobs. Again.

In this fraught context, it is hard to improve upon the words of Pat Buchanan, who has few peers in diagnosing what has happened during the 44 years since Watergate and where this second exercise by the nation’s elites in reversing the will of the people might lead:

What will be the reaction out there in fly-over country, that land where the “deplorables” dwell who produce the soldiers to fight our wars? Will they toast the “free press” that brought down the president they elected, and in whom they had placed so much hope?

My guess: The reaction will be one of bitterness, cynicism, despair, a sense that the fix is in, that no matter what we do, they will not let us win. If Trump is brought down, American democracy will take a pasting. It will be seen as a fraud. And the backlash will poison our politics to where only an attack from abroad, like 9/11, will reunite us.

In the midst of a financial crash and unexpected recession, the Imperial City will degenerate into a permanent Gong Show. It will not be able to fund the American Empire abroad or agrees on how to stage an orderly retreat. Foreign policy will lurch and flip-flop dangerously.

At the same time, attempting to fund the nation’s bloated Welfare State and government driven health care system in the face of a doubling of the retired population over the next several decades will prove impossible. The funding, borrowing and taxing crisis will be fractious and non-stop.

The only certainty is that there will never be another meaningful tax cut because once the demise of the Orange Swan comes into play it will not be remotely possible to assemble a Congressional majority for revenue neutral reform or to raise the debt ceiling high enough to accommodate a Reagan-style deficit financed cut.

So that’s what we mean by regime change—homeland edition. The nation is heading into a fiscal dystopia that the central bank can not possibly fix or even ameliorate. It shot its wad inflating two giant financial bubbles after the Dotcom crash—–ending first in the 2008 mini-meltdown and now in the real one of 2017-2018. Now it is out of dry powder, credibility and any new ways to print money.

As the Donald himself tweeted yesterday, what is happening is indeed hard to believe:

Hard to believe that with 24/7 #Fake News on CNN, ABC, NBC, CBS, NYTIMES & WAPO, the Trump base is getting stronger!

That may be—-even if the polls don’t show it. Yet Trump’s “base”—- impaled in its daily struggles to make ends meet– won’t save him from the combined assault of the Deep State, the mainstream media, the partisan Dem attack machine and the careerist GOP politicians of Capitol Hill who are simply waiting for the Donald to essentially fall on his own sword.

But that won’t end the Fake News. It will only end the Fake Quiet that hovers in front of the greatest financial and political storm ever.

Reprinted with permission from David Stockman’s Contra Corner.