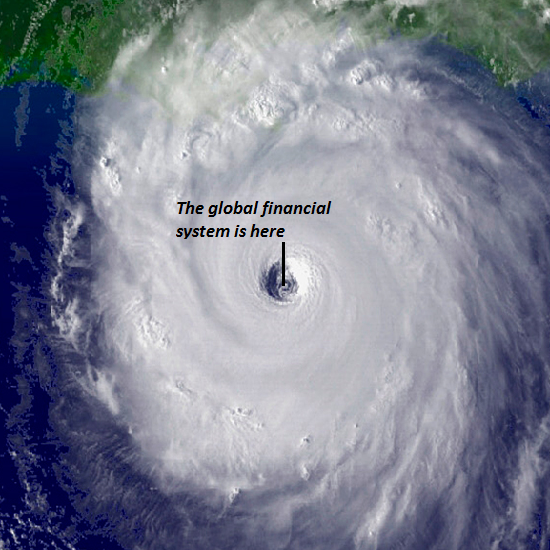

We're in the Eye of a Global Financial Hurricane

May 25, 2016

The only “growth” we’re experiencing are the financial cancers of systemic risk and financialization’s soaring wealth/income inequality.

The Keynesian gods have failed, and as a result, we’re in the eye of a global financial hurricane.

The Keynesian god of growth has failed.

The Keynesian god of borrowing from the future to fund today’s consumption has failed.

The Keynesian god of monetary stimulus / financialization has failed.

A Radically Beneficial...

Best Price: $8.45

Buy New $1.99

(as of 05:25 UTC - Details)

A Radically Beneficial...

Best Price: $8.45

Buy New $1.99

(as of 05:25 UTC - Details)

Every major central bank and state worships these Keynesian idols:

1. Growth. (Never mind the cost or what kind of growth–all growth is good, even the financial equivalent of aggressive cancer).

2. Borrowing from the future to fund today’s keg party, worthless college diploma, particle board bookcase, stock buy-back, etc. (oops, I mean “investment”)–a.k.a.deficit spending which is a polite way of saying this unsavory truth: stealing from our children and grandchildren to fund our lifestyles today.

3. Monetary stimulus / financialization. If private investment sags (because there are few attractive investments at today’s nosebleed valuations and few attractive investments in a global economy burdened with massive over-production and over-capacity), drop interest rates to zero (or below zero) to “stimulate” new borrowing… for whatever: global carry trades, bat guano derivatives, etc.

Here is my definition of Financialization:

Financialization is the mass commodification of debt and debt-based financial instruments collateralized by previously low-risk assets, a pyramiding of risk and speculative gains that are only possible in a massive expansion of low-cost credit and leverage.

The Gulag Archipelago ...

Best Price: $5.46

Buy New $11.39

(as of 05:20 UTC - Details)

The Gulag Archipelago ...

Best Price: $5.46

Buy New $11.39

(as of 05:20 UTC - Details)

That is a mouthful, so let’s break it into bite-sized chunks.

Home mortgages are a good example of how financialization increases financial profits by jacking up risk and distributing it to suckers who don’t recognize the potential for staggering losses.

In the good old days, home mortgages were safe and dull: banks and savings and loans institutions issued the mortgages and kept the loans on their books, earning a stable return for the 30 years of the mortgage’s term.

Then the financialization machine revolutionized the home mortgage business to increase profits. The first step was to generate entire new types of mortgages with higher profit margins than conventional mortgages. These included no-down payment mortgages (liar loans), no-interest-for-the-first-few-years mortgages, adjustable-rate mortgages, home equity lines of credit, and so on.

This broadening of options (and risks) greatly expanded the pool of people who qualified for a mortgage. In the old days, only those with sterling credit qualified for a home mortgage. In the financialized realm, almost anyone with a pulse could qualify for an exotic mortgage.

The interest rate, risk and profit margins were all much higher for the originators. What’s not to like? Well, the risk of default is a problem. Defaults trigger losses.

Hillary Wants You To Drive 55

Hillary Wants You To Drive 55