When and where were you…when you were jolted to reality by the clarity of the thoughts of Austrian-school economists and libertarians like Murray Rothbard?

I was in high school in the mid-1960s and the jolt propelled me through college and into graduate school in the early 1970s. It was as if I had attached myself to rockets. And indeed I had.

Like many back then, the trajectory was unquestionably toward academia – and a career in university teaching and furthering what we had learned from those minds. But alas, I deviated.

The mid-1970s depression delayed many academic careers as hiring at universities ground to a halt. In my case I jumped ship from a Ph.D. program at Univ. of Hawaii and went to E.F. Hutton (N.Y.C.) as a gold futures specialist – back when that market was “legalized by the authorities” in 1975. I was going to latch myself to that anti-statist commodity and it would be simple – the metal that would ultimately supplant the various fiat currencies with a dose of reality, and I was going to be at least one of its spokesmen on Wall Street. Little did I know at the time. I learned.

[amazon asin=146793481X&template=*lrc ad (right)]

The ride from there to here was a long one, bumpy and full of ever increasing cycles of ups and downs, and not merely by gold. All asset categories have undergone boom-bust cycles over the past 30 and more years. And now those cycles are looking more and more like terminal heart-attack oscillations.

And despite being what I regard as very knowledgeable about libertarian concepts, free market theory, and so forth, I have learned some things that are somewhat “outside” of our mutually-shared view of markets, men and the State. I pass some observations along.

The capital raising and lending business (broker-dealers, banks, etc.) are to the popular culture what “capitalism” is or at least what they think it is. But in truth the financial/investment industry is fully split, as is the broader culture, between those who respect and understand the concepts of a free market and those who are quite frankly the lapdogs of the State, of the Fed and the ideology of the State. You can see a fair sampling of this intellectual division on CNBC – for example the difference between Rick Santelli on the one hand (who in his 2009 on-air rant, declared the need for a “tea party”) versus CNBC’s Fed analyst, Steve Leisman, who rarely ever does more than laud the actions of the Fed. This divide is not merely one of a marketing contrivance by CNBC, to offer a false “balance,” but is in my opinion a real divide in the financial arena – hedge funds, mutual funds, banks, brokers etc. – that actually buy and sell on Wall St. And these “players” are probably less-balanced in their view of the Fed than are the talking heads. The reason is that even those who presumably “know better” are in effect forced into the path set by the Fed. Such that investors and asset managers that are obediently following the Fed’s breadcrumb trail even include asset managers who often confess on financial TV that “all of this will end badly.” Yet they are forced to go with the tide and they do. And so, willy-nilly, the Fed-loving asset managers and the Fed-doubting asset managers alike are channeled into buying stocks (that’s the current stated Fed goal, somewhat different from prior boom bust cycles). And in so doing the blue chip U.S. stock indexes have outpaced on the upside all indexes worldwide, over the past two years in particular. An outpacing and out-pricing that has no historical comparison. For example just by referencing current S&P500 price level versus its highs in early 2011 (a point when most stock indexes suffered a sharp pullback) its action is more than 20% above that high, whereas most indexes globally remain below that high and only a few (FT-100 in London and DAX in Germany) are marginally out above that peak. In sum, the Fed has “succeeded” in its stated goal of driving stock prices up, with the ulterior motive of creating a “wealth effect” among U.S. investors. An openly declared effort to fake reality. In my professional assessment the current U.S. stock market is now clearly a phenomenon which can be defined and measured many ways – as a bubble of great excess. The axiom is “You can’t fight the Fed.”

The reason that asset managers “must” play the game is that the more fearless (mindless) among them have already committed themselves headlong into the Fed-led buying frenzy and have gained nicely in so doing. Generally this feeding commenced around the time of the QE2 announcement in August, 2010 – three years ago. Those who doubted or were reluctant in their commitment to Fed-chasing were marginalized in the constant peer assessment process that’s called “relative performance.” If you were not up-to-the-eyeballs-long stocks, especially U.S. stocks, then you were not being benefited by the Fed’s largesse, and you soon learned your lesson as your clients, one-by-one, peeled away to sign-up with the “better performers.” One herd then joined by another, and it persisted, and in so doing has further perpetuated the myth of the omnipotence of the Fed.

Another thing I have learned in the past 37 years, and have to some extent be able to measure with some precision, is the absolute and recurring failure of herd-like, trend-following behavior by those who act upon the Fed axiom. Meaning, to you Austrians and libertarians out there who think you have your concepts in order, you do. Please do not be doubtful of your intellectual foundation, nor dismayed by the ability of this Fed-led game to persist for so long and to create so many rewarded followers. And especially I say to the many young new students of Austrian-school economics and of libertarianism – you are only just now seeing probably your first major example of a boom-bust cycle. Do not doubt your concepts because of the “fact” that your young investing buddies are making money by acting upon “the Fed is invulnerable” axiom. It has happened before and is now happening again, though this time around it could very well be different in terms of the significance of the consequent bust. More on that in a minute.[amazon asin=1491068620&template=*lrc ad (right)]

There is a lesson that market history has clearly and repeatedly demonstrated, at least all the years I have been technically analyzing markets (and during which time I have kept my libertarian mode of assessment at arms-length from my proprietary technical measures). The lesson is that the Fed, depending upon its commitment and duration (and I should include Federal government policies in this process as well, such as the Clinton “single family home for everyone” policy) does create excess. And that’s the point. It does create excess pricing and trends that “would not otherwise be” had it not been for its manipulations of the unit of measure, the money unit – sometimes dramatic manipulations. These policies persist not because they are viable, but because they come from the barrel of the gun of the State. To some extent they are unavoidable. And like any coercive homogenizing policy they are believed in by many who follow in their wake. And in the early and middle phases of these booms those who do follow are rewarded. Therefore it is often the case that these policies will in fact generate “trends” that attract many, and which persist over sufficient periods of time to create the veneer of “sustainability.” The early doubters become late joiners, again because of the peer group “performance” pressures that come in the wake of such policy-driven trends.

Ask the “investor” who thought he had found a career in “flipping” homes in 2006 and 2007. He might have been a late-joiner, following some buddies who showed him the way, but he, like even some of the reluctant and more sober banks, finally joined-in the mortgage orgy (for the banks it was the bundled MBS orgy) of those years. And yes, they paid dearly for their belief structure – a wholesale discounting in price of their asset category. Yet that was just another massive market trap in a parade of such bubbles that have been sponsored by Fed action over the past handful of decades and longer. And, of course, it lasted just long enough to make it seem inevitable and sustainable. Those are the recurring attributes of this process – attributes which must be acknowledged and “respected.” Excess trend and the perception of sustainability of that trend. They are almost prerequisites for the great unwinding. Beware and respectful of the process that the Fed creates. Yes, it is a distortive and is a false process, but in its early and middle phase it “works”…up to a point. This lesson about market place reality is one that contains the alternative to the Fed axiom. That alternative axiom can be expressed in several ways, but I prefer “You can’t fool mother nature!” (meaning the markets). At least not forever. And if you think you have done so – if you have a sense of assuredness regarding your Fed-sponsored asset market – and if that cocky smile is now widely spread among other investors and asset managers, then in all likelihood the comeuppance is near.

Now I will get down to more specifics – namely market-related macro-trend technical specifics. In measuring the U.S. stock market (using the Dow Industrials and the S&P500) and going back over 90 years, I have found the following archival record of trend behavior, remembering of course that many of the trends in the market, including that of the late 1920’s, were heavily influenced by actions of the Fed (for example, see Rothbard’s America’s Great Depression, chapter 4, “The Inflationary Factors,” regarding Fed monetary policy during the 1920’s bull market).

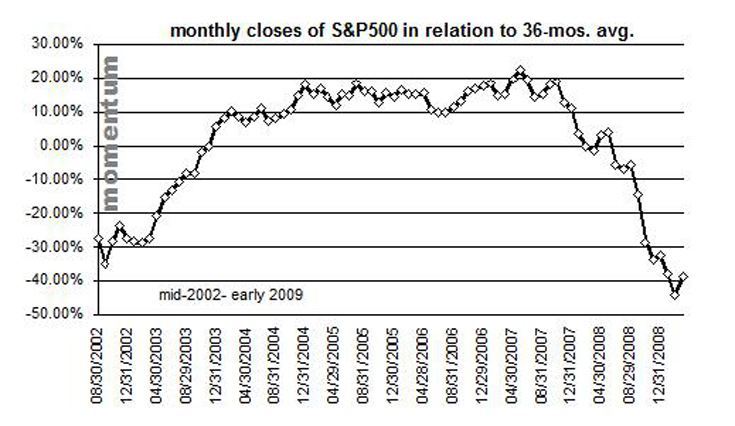

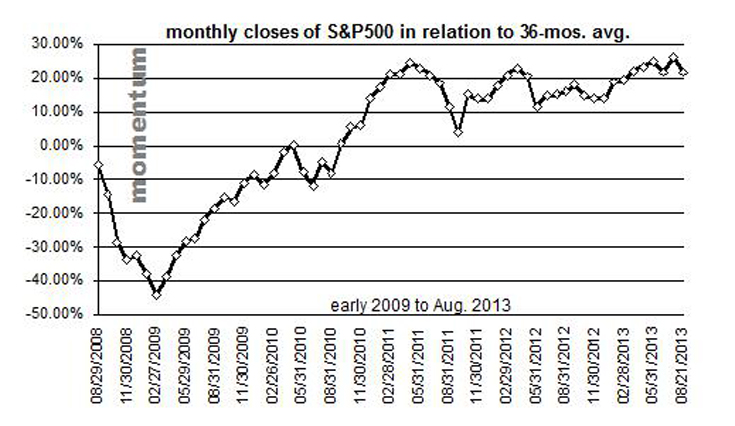

First, I measured trends in the market in their relation to a long term mean, specifically a 36-mos. average. I then measured each monthly close in relation to that average. In a bull trend these readings would of course show as an advance in price in relation to that 3-year average, and when plotted on an oscillator would show as upticks. Any deviation in those readings which amounted to a 30% contrary move I would regard as a full termination of the prior trend – hence would define a new trend direction for purposes of my counting of the momentum trend clock. The average trend lasted 29 months before it was then negated by a movement of sufficient percentage in those readings in the opposite direction.

The 3 oldest trends in U.S. stock market history, as measured by my annual momentum-based method, were the bull markets that ended in 1929, 1987 and 2007. The 1929 bull market and 1987 peak were both 5 years and 1 month old (measuring from the low monthly momentum reading of the preceding bear market). The 2007 peak was 4.5 years old at its momentum peak (chart below). Very aged trends, well above average maturity. And age is a factor as much as price in measuring excess. It is not surprising that these 3 very aged bull trends produced in turn the 3 largest, sharpest and most rapid collapses in U.S. stock market history.

Well, all you Fed chasers out there, my measurement of the current bull trend (chart below) puts it now into that rare group of very aged bull trends – it just passed 4.5 years, measuring from the lowest monthly closing reading of the last bear market (Feb. 2009). Can it sustain for longer? Sure. But one must be aware that the clock is not only getting old but its price behavior (versus other asset categories and versus other major developed market stock indexes) is at historical excesses as well. These two factors, among others, argue that the fuse is short; the game has likely run or nearly run its course. I strongly suspect that we will see soon (within weeks or a handful of months) that yet again another Fed-sponsored bull trend has expended itself and done so in its normal fashion – old, excessive beyond credibility, full of exuberance, and now with a sense among many of its “sustainability.”

The question then will be, what does the comeuppance look like? How fast, how deep, how painful? If my archival findings are even a reasonably fair template, the consequence will not be “good.” But it will be “fair” (meaning a justified balancing of the scales) and will likely involve a full erasure of the prior price trend – which was the case and then some with each of the prior 3 oldest and most excessive bull trends in U.S. stock history.

A final observation, not technical. Prior excuses for Fed interventions involved supposed greed and errors caused by market factors. Such as the myth of the 2008 collapse being caused by greedy and stupid Wall St. banks and broker-dealers. The Fed (and the central government) then swoops in, armed with those headlines, and manipulates the markets in whatever desired direction its great wisdom of the “ought” leads it. And in the past, few observers objected to Fed policies, because as we all “know” if it weren’t for the Fed, for example in 2008 and 2009, we would be a great depression now!

This time, I argue the situation is different. The central banks of the developed world are no longer defending against private failure but are shoring up their own defenses. The chickens have come home to roost. It’s their policies which, if they fail (when they fail), will bring into great doubt the viability and potency of central banks. Already, even among a growing number of non-free market mainstream economists, there is a sense that the Fed is actually impotent and/or distortive in its policies. Yes, stocks are up, but no real world measures reflect the stock market’s trend. Failure now – as exemplified by a failure in stock market uptrend – will turn the spotlight fully on the Fed. The perception already is that stocks would not otherwise be where they are now if it were not for Bernanke’s goal of driving stocks upward. It is the only victory he can claim, and if that victory vanishes, especially with speed and some noise, the Fed will be stripped bare of its robes – of potency, effectiveness and necessity of being. The Fed axiom will die abruptly.

And in this regard, free market advocates should sit back and appreciate the historical excesses that the Fed has pushed the situation. It is by virtue of its excesses, in the past and now, that it generates the massive counter moves – the busts. This time the Fed will not be able to blame banks, brokers and businessmen for a decline. Most will realize (with a few exceptions such as the Krugmans of the world) from whence it came. This could very easily be the Final Game. This could be the bust that is and was pre-explained by Austrians and libertarians, hence will serve to boost that body of thought into even wider acceptance. Enjoy. We cannot change what the State has done; we can only analyze and explain its consequences to those who for so many decades have seen this process of boom-bust repeat itself without an understanding of its causes and dynamics. No mystery any more.