We are now in the month of April—–so the Wall Street Keynesians are back on their spring “escape velocity” offensive. Normally they accept the government’s seasonal adjustments in stride, but since Q1 is again hugging the flat line or worse, it seems that “bad seasonals” owing to an incrementally winterish winter explain it all away once again. Even today’s punk jobs number purportedly reflects god’s snow job, not theirs.

What’s really happening, they aver, is that jobs are booming, wages are lifting, housing prices are rising, consumer confidence is buoyant, car sales are strong and business is starting to borrow for growth. In fact, everything is so awesome that one Wall Street economist quoted yesterday could hardly contain his euphoria:

“Consumers have emerged from the winter blues. If they spend anywhere as great as they feel right now, then this economy is going to roar over the next few months,” said Chris Rupkey, chief financial economist at MUFG Union Bank in New York.

Meltdown: A Free-Marke... Best Price: $0.25 Buy New $20.00 (as of 02:20 UTC - Details)

Since Rupkey has been expecting a roaring economy for several years now it is tempting to dismiss his latest fantasy as just the institutional cluelessness which emanates from the pitiful behemoths which pass for Japanese banks. But with only slightly more enthusiastic bombast, Rupkey is simply braying from the generic Wall Street script.

Since these people get paid a lot, have PhDs and might even be smart, how is it that they are so wrong, and have been now for five years running? There is a simple answer: They are operating on a business cycle model that is utterly erroneous and obsolete; and which therefore distorts and obfuscates the ‘in-coming’ data and the inferences and forward expectations that they derive from it.

In a word, their father’s business cycle model was premised on a “clean balance sheet” world driven by main street borrowing. In fact, however, we have now passed through the “peak debt” horizon and are in a bubble finance world driven by Wall Street speculation. That passage changes everything.

To be sure, the old fashioned main street cycle was the work of the Fed no less than today’s. After all, the business cycle itself is essentially a product of central banking.

Indeed, central banks function akin to the 12-year old who killed his parents and then begged the court for mercy on the grounds that he was an orphan. That is, they inherently generate credit inflations and the resulting economic boom and bust—–only to then claim indispensability in reversing the recessionary slump and avoiding a plunge into depressionary darkness.

But there were some big differences between then and now. The Fed of yesteryear was reactive, prudent and pre-Keynesian. It occasionally raised interest rates to “lean against the wind” in the event of too much economic boom and rising inflation; and it moderately lowered rates and loosened monetary conditions once inflation had abated and idle labor and capital resources had become too large. But mostly it was a passive watchman.

Stated differently, the gentle hand of modest federal funds rate adjustments over a few months time designed to lightly guide the macro-economy is one thing. Today’s heavy handed 75-month stretch of ZIRP and chronic financial repression aimed to control, manage and manipulate the short-run path of GDP is quite another.

Likewise, back then we had what amounted to central banking in one country—-something very different than today’s globally synchronized convoy of Keynesian central banks all racing in the same direction of ease and rampant money printing. So too, US labor costs were on par with the rest of the mainly European industrialized world versus today’s billion-plus pool of cheap labor in China and the EM.

Most importantly, back then household balance sheets were relatively unleveraged, enabling a robust response to changes in the price of credit and a consequent mobilization of consumer spending. By contrast, for 80% of today’s debt saturated household balance sheets, spending is essentially constrained to current wages and income regardless of the price of credit.

Finally, the old time capital markets were relative honest, which meant that debt and equity capital were priced correctly and that executives were rewarded for investing in long-term productive assets. Needless to say, that’s light years of difference from today’s utterly dishonest financial casino’s where debt is drastically underpriced and financial engineering maneuvers like stock buybacks and M&A deals are deeply subsidized and powerfully rewarded.

The Big Short: Inside ...

Best Price: $1.49

Buy New $7.99

(as of 02:35 UTC - Details)

The Big Short: Inside ...

Best Price: $1.49

Buy New $7.99

(as of 02:35 UTC - Details)

These profound differences have caused the Fed-influenced business cycle to play out far differently. In the 1960s and 1970s, for example, cutting interest rates caused housing starts and business investment to boom. Then when credit-fueled demand got way ahead of supply——wages and prices tended to accelerate sharply. You got “inflation in one country” because there was no mobilized cheap labor pool and export factories in Asia to constrain the classic wage-price-cost spiral.

Yes, there was industrial trade, but European wage levels and union-based adjustment rigidities tended to parallel those in the US, and therefore did not really function as an economic circuit breaker. So eventually, the Fed had to throw on the brakes in order to extinguish the very wage-price spiral it had triggered in the first place.

After Nixon’s destruction of the Bretton Woods gold exchange standard at Camp David in August 1971 and the elimination of the modest financial discipline that it provided, the Fed’s impact got more intense and the business cycle far more volatile. As shown below, when the Nixon-Burns regime threw open the monetary spigot in the run-up to the 1972 election, the economy boomed initially because the response to cheap and abundant credit was fast and furious.

But it soon led to a rip-roaring wage and price spiral not withstanding the clumsy system of wage and price controls that the Nixon Administration had also launched at Camp David. And it is crucial to understand how and why that played out so differently back then——compared to the allegedly inflationless tsunami of money printing today.

The big difference was no China, no endless rice paddies and rural villages that could be drained of cheap labor and mobilized into the world’s commercial economy. China’s incipient billion person anti-inflation force was starving in the rural villages owing to the calamites of the Great Leap Forward, where villagers had dutifully melted-down their hoes and plows to make backyard steel, and the Cultural Revolution, which had paralyzed economic life entirely.

So what happened was US imports soared after domestic capacity was fully used-up, touching off a world-wide boom in both investment and consumer goods. That, in turn, generated an explosion of oil and other commodity prices as world demand for raw materials temporarily outran the existing supply base.

Next, soaring oil and other commodity prices flowed back into the US economy, touching off a domestic wage and price spiral that fueled itself. In the face of rampant demand and no China hammer on wages and prices of tradable goods, its was only the Fed’s slamming on the brakes in late 1973-1974 that finally broke the inflationary tide.

Accordingly, the profound difference in the Fed’s money printing cycle then and now is crucial to understand. The following excerpt from the Great Deformation captures the essence of what happened in that post-Camp David, pre-China interval:

So what transpired during the early years of floating was a massive worldwide expansion of money and credit fueled by the Fed. This, in turn, generated the greatest bout of commodity price inflation that the world had seen since the postwar fly-up in 1919.

Crude oil led the way. Having been priced on the world market at $1.40 per barrel when Nixon’s free marketers gathered at Camp David in August 1971, it rose to an interim peak of $13

The Great Deformation:... Best Price: $4.26 Buy New $8.99 (as of 05:50 UTC - Details)

The dramatic post-1971 escalation of worldwide oil prices was blamed by officialdom on political rather than economic forces—and in particular the alleged market rigging of the OPEC cartel. In fact, except for a brief period around the October 1973 Mideast war, there was no systematic withholding of oil from the market.

The problem was not a shortage of oil but a flood of money and inflated demand. During 1972–1974, the global economy reached a red-hot pace of expansion, which in some part was due to the locomotive pull of the Nixon boom. For example, non-oil imports to the United States rose by 15 percent in the first year after Camp David, and then accelerated to 22 percent growth the next year and 28 percent during the twelve months ending in August 1974. These giant gains in imported goods were literally off the charts.

So as blistering US demand ignited production booms around the world, factory operating rates rose and supply chain backlogs surged everywhere on the planet. Moreover, there was another entirely new, even more potent force at work. In response to the Fed’s flood of money and credit, other central banks around the world reciprocated with their own fulsome monetary expansion.

They bought dollars and sold their own currencies in foreign exchange markets in order to forestall the upward pressure on exchange rates that was inherent in the brave new world of floating currencies. In other words, the heretofore circumspect central bankers of the world became furious money printers in self-defense as they faced the flood tide of dollars beingissued by Arthur F. Burns.

In fact, with exchange rates no longer fixed and visible, a more subtle process of competitive devaluation became the daily modus operandi of the system. In this manner, the Fed propagated its inflationary monetary policies outward to the balance of the world economy.

So it was a storm of money and credit expansion which generated the first commodity bubble after 1971, not the OPEC cartel alone or even primarily. For if the problem had been just the putative rigging of prices by the oil cartel, there is no way to explain the dozens of parallel commodity booms during the same two- to three-year time frame.

Quite obviously, there was no evidence of cartel arrangements in the markets for rice, copper, pork bellies, or industrial tallow, for example. Yet between 1971 and 1974, rice rose from $10 to $30 per hundredweight, while pork bellies climbed from $0.30 per pound to $1.

Likewise, the cost of a ton of scrap steel soared from $40 to $140; tin jumped from $2 to $5 per pound; and the price of coffee rocketed up nearly eightfold, from 42 cents to $3.20 per pound. Even industrial tallow caught a tailwind, rising from $0.06 to $.0.20 per pound, and pretty much the same pattern was reflected in the price of corn, copper, cotton, lead, lumber, and soybeans.

Needless to say, the first inflationary cycle of floating money came as a shock to policy officials, especially the Federal Reserve and its chairman. While Chairman Burns was a pusillanimous accommodator when it came to the game of hardball politics in Washington, as a matter of belief he had remained an anti-inflation hawk.

The Real Crash: Americ... Best Price: $3.00 Buy New $9.55 (as of 12:25 UTC - Details)

So when Nixon went into his terminal Watergate descent, Burns got his nerve back and threw on the monetary brakes. Accordingly, double-digit bank credit expansion came to a screeching halt, rising by only 1.2 percent in 1975.

As it happened, the Fed’s stimulus had worked spectacularly from a macro perspective because households had been able to borrow hand over fist to buy cars and new homes. This credit based spending surge, in turn, touched off a virtuous cycle of income and jobs gains, more spending and even more consumption.

Thus, new home construction boomed. Housing starts initially more than doubled during the three years after 1971. Then when the Fed was forced to rein in the cycle with sharply higher interest rates owing to the soaring CPI and wage inflation, construction instantly collapsed—–only to re-erupt after the Fed returned to an easing mode in late 1974.

![]()

The same pattern can be seen in the case of real business investment, where the cyclical fluctuation was even more extreme. When the Fed opened the credit spigots in 1971, net real investment in plant and equipment soared by 52% during the next two years, but then plunged by nearly 45% from the 1973 peak when the Fed was forced to close the credit spigot.

Needless to day, after the 1974-1975 easing cycle incepted, the cost of business credit fell sharply and investment spending boomed once again. In fact, real net business investment rose by 100% between 1975 and 1978—–a record never duplicated before or after.

![]()

Absent the China price, of course, wages and CPI inflation followed the same cycle because there was no ultra-low cost production alternative. That is, no place to “off-shore” production and to arbitrage labor costs. Accordingly, the Fed had no choice except to throw on the brakes twice during the decade because these vicious spurts of wage and price inflation created instant and widespread cost-of-living pain on main street.

How an Economy Grows a...

Best Price: $1.99

Buy New $7.20

(as of 11:05 UTC - Details)

How an Economy Grows a...

Best Price: $1.99

Buy New $7.20

(as of 11:05 UTC - Details)

Thus, when the Nixon-Burns money printing spree incepted in late 1971, the CPI was increasing at about a 3% annual rate, but had soared to 12% by November 1974 at the height of the global boom. After the Fed threw on the brakes and sent the US economy into a tailspin, the rate plunged to under 5% by late 1976. Then, under a renewed burst of Fed stimulus and breakneck credit expansion, CPI inflation soared to nearly 15% by early 1980.

At the end of the day, this was the inflationary blow-off that finally discredited old-fashioned Keynesianism and brought Ronald Reagan to office. And once again, the reason for the late 1970s consumer price explosion was not the presence of OPEC in the world oil market; it was the absence of the China labor force and the “china price” for tradable goods in the face of massive monetary expansion.

US Inflation Rate data by YCharts

Two big things changed after 1979-1980. First, the Maoist founders were run out of China and replaced by “red capitalists”. The latter soon discovered that state power actually flows from the end of a printing press, not the barrel of a gun.

Amazon Prime (One Year...

Check Amazon for Pricing.

Amazon Prime (One Year...

Check Amazon for Pricing.

Secondly, the White House staff finally bamboozled Ronald Reagan into getting rid of Volcker. The latter development ushered in Greenspan and the age of financial repression; the former development empowered Mr. Deng and his export factories, thereby triggering the age of the China price and global wage repression.

The rest is history and is memorialized in the two graphs below. In a word, Greenspan and his successors massively exported the inflationary impact of their policies, especially before the 2008 financial crisis.

On the one hand, they expanded domestic credit like never before, causing US credit market debt outstanding to rise from $11 trillion when Greenspan took office to $52 trillion when Bernanke falsely told panicked Congressmen in September 2008 that we were on the cusp of Great Depression 2.0.

Folks, that’s a 5X increase in barely two decades or a credit growth rate of nearly 10% annually.

![]()

Yet unlike the 1970s, there was no inflationary blow-off because the massive domestic spending fueled by the Fed’s printing press was absorbed by China and its EM supply base. Indeed, since the 1980s the US has run cumulative current account deficits of nearly $8 trillion——–consumption which was supplied from outside the four walls of the US economy and therefore did not fuel domestic inflationary pressures.

![]()

But, no, this wasn’t a case of Adam Smith’s division of labor and miracle of free trade. Nor was it a financial free lunch. Instead, this was classic vendor finance——but on an epic scale.

China, the Persian Gulf oil producers and the rest of the EM loaned us the money by running their own printing presses and buying up dollars to suppress their exchange rates and protect their mercantilist trade model. This allowed the US household sector in particular to bury itself in debt before the normal, historic mechanism of soaring interest rates could choke off the borrowing binge.

Effectively, the Greenspan-Bernanke era of massive financial repression caused the subtle and flexible tool of credit price rationing to be displaced by a blunt instrument. Namely, balance sheet saturation or “peak debt”. After 2008, households stopped borrowing because they had exhausted their capacity to carry any more debt relative to income. As shown below, household leverage ratios have actually begun to climb down from the nosebleed section of history where they had been carried in the final wave of the credit boom before the 2008 crisis.

Household Leverage Ratio – Click to enlarge

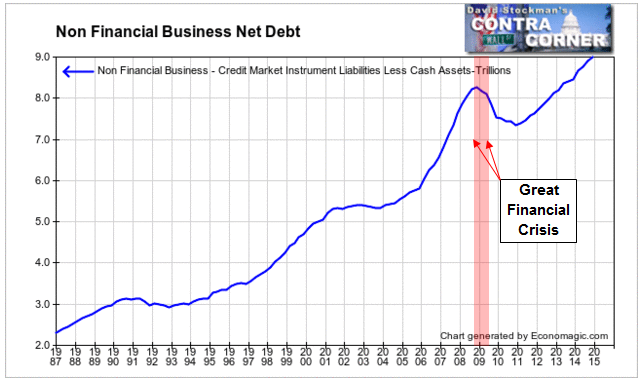

On the business side, the data trends are slightly different, but the impact is the same. Both gross and net business debt have continued to rise since 2007, but the proceeds have been almost entirely recycled into financial engineering—including more than $2 trillion of stock buybacks and many trillions more of basically pointless M&A deals.

This diversion of the $2 trillion gain in business debt outstanding since 2007 to financial engineering is owing to the near zero after-tax cost of corporate debt. The latter has caused the enslavement of the C-suite to the instant gratification of rising share prices and stock options value in the Fed’s Wall Street casino.

Non Financial Business Net Debt- Click to enlarge

The bottom line is therefore straight forward. The credit channel of monetary policy transmission is now broken and done. The impact of ZIRP and QE never leaves the canyons of Wall Street——meaning that it functions to inflate financial assets rather than main street wage and prices as it did during the era of inflation in one country.

But that makes for both a considerable irony and an incendiary danger. Today’s clueless Keynesian central bankers essentially believe that they can keep the pedal-to-the-metal until a 1970’s style inflationary spiral arises. But none is coming because the worldwide central bank money printing spree of the last two decades has generated massive excessive capacity and malinvestment all around the planet. What is coming, therefore, is not their father’s inflationary spiral, but an unprecedented and epochal global deflation.

So the central banks just keep printing, thereby inflating the asset bubbles world-wide. What ultimately stops today’s new style central bank credit cycle, therefore, is bursting financial bubbles.

That has already happened twice this century. A third proof of the case looks to be just around the corner.

Reprinted with permission from David Stockman’s Corner.