“That’s money in the bank” is on old expression of the surety of the value of money housed inside a banking system. But today savers are being clobbered by less than 1% interest being offered on saved money + erosion of purchasing power due to inflation.

Charles Schwab, the investment guru, speaking out in The Wall Street Journal, bemoans the low interest rates on saved money that has affected so many retirees. Schwab is calling for the nation’s central bank (The Federal Reserve) to raise interest rates.

While Schwab estimates that the loss of interest income is $58 billion in annual income since 2008 ($348 billion total), that figure is much higher when the real inflation rate is factored.

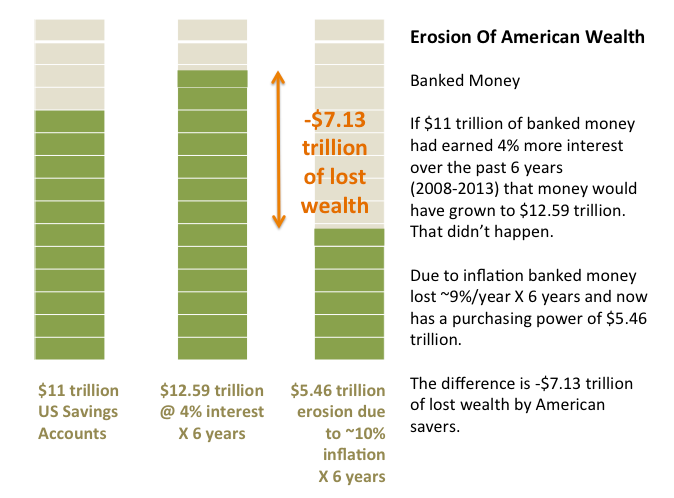

Schwab says there is $11 trillion in short-term accounts bearing very low interest. Schwab doesn’t reveal all of the numbers used in his calculations, but let’s say he was factoring the difference between 5% interest versus the less-than-1% now offered, for a difference of ~4%. On a compounded basis, that would amount to a loss of ~$2.915 trillion of interest income (mercy!) over the past 6 years.

The erosion of wealth due to inflation adds to the problem. It is economist John Williams of ShadowStats.com who shows the real rise in inflation (cost of living) is closer to 10% rather than the central bank’s target inflation rate of ~2.2% which matches the Bureau Of Labor Standards questionable inflation numbers. (ShadowStats.com)

While Federal Reserve chairman Ben Bernanke said the economy was recovering, his bank was masterminding the robbery of trillions of dollars from American savers while bragging the Fed was keeping interest rates low that (a) created a false bubble in the real estate market; but (b) managed to keep interest on the national debt low ($400 billion on $17 trillion).

As an aside, if the Federal Reserve raises base interest rates to 5.0% on the national debt rather than the 2.3% interest rate on that borrowed money today then annual interest on the national debt would rise from $400 billion to ~$850 billion and virtually throw the nation into insolvency.

So the Federal Reserve is stuck between a rock and a hard place. If the Fed comes to the rescue of savers it demolishes the ability of the Federal government to meet its obligations to make interest payments on its $17 of accumulate debt.

The nation generates ~$2.4 trillion tax revenues and $850 billion in interest payments would mean the country would be paying 35.4% of its revenues just in interest payments on the national debt.

But getting back to our calculations of lost income of American savers, it is John Williams at ShadowStats.com who calls attention to the chicanery of the Federal Reserve that uses sleight of hand to calculate the rate of inflation. If inflation were calculated the way it was done in 1980 then the real rate of inflation is closer to 10% (~9.6% according to Williams. (ShadowStats.com)

So savers not only lost income from interest payments but their money also lost purchasing power.

Schwab’s estimated $58 billion of money that savers were deprived of represents less than a 1% loss of income per year on $11 trillion (about 0.0052% or one half of 1%). So let’s calculate that savers not only lost interest income but purchasing power as well.

Savers in the period 2008-2013 have been losing ~4% on the + side due to low yield interest rate accounts and ~9% on the – side due to inflation.

So $10,000 in the bank @5% extra interest/year X 6 years would grow that money to $12,653 over that time. (CalculatorSoup.com) But your $10,000 of savings grew by less than 1% (let’s just round off and call it 1%), so it only grew to $10,615 over that six-year time period, for a difference of $2038 of lost income.

Additionally, the purchasing power of your banked money lost ~9% annually lost ~$5393 in purchasing power over that time. (ShadowStats.com inflation calculator) Goods and services that cost $10,000 in 2008 amounted to $15,593 in 2013.

Your $10,000 of saved money in 2008 would have lost $2038 in income due to low yield interest rates and $5393 in purchasing power over that six-year time period. That is a total loss of over $7000 from a starting point of $10,000.

For every $1 trillion in the bank, US savers lost $153.9 billion/year X 6 years = -$923.4 billion X 11 ($11 trillion in US bank accounts) = $5,540,000,000,000 or $5.54 trillion in purchasing power! Additionally savers lost $1.590 trillion in low yield interest accounts. Folks, American savers have been fleeced! Ten thousand dollars of banked money in 2008 could have risen to $12,653 at 4% interest income but lost over half of its purchasing power over that 6-year period of time vaporized to less than $3000 by the year 2013.

The Federal Reserve chose to rob from savers to bail out the Wall Street investment class.

Another $6 trillion was lost by American homeowners over this same time period. (CNNMoney.com June 2011)

Good God, Americans have incurred unprecedented erosion in the value of their savings over this time period.

All the while, the news media, being minions for the banking class, chide Americans to save more money. (CBSNews.com) (What, and lose their shirt?)

Meanwhile, over the past decade, American wages have stagnated. (TheEconomist.com Sept 6, 2014)

Some economists argue that the income of Americans has risen significantly when you figure for increased health benefits, vacation pay, etc. (CNBC.com Jan 29, 2014)

But these economists use the government’s phony inflation numbers and not every American works for a company that offers these benefits, certainly not the self-employed. Because health insurance is partially paid for does not mean American families can pay the rent or buy groceries.

Over half of American wage earners today make no more than $20/hour. (MarketWatch.com Nov 17, 2014)

Americans earning $20/hour in 1980 ($38,400/year) would need to make $58/hour today ($111,360) to make up for inflation (US Inflation Calculator) Less than 5% of American workers make that much money per hour today.

And you wonder why the Presidential candidate Ron Paul campaigned to “end the Fed?”